The US faces some tough challenges in increasing domestic oil and gas production beyond 2030, according to a new report by Wood Mackenzie.

“Tough at the Top: The Threats to US Energy Dominance,” announced on 17 April, said even if demand for oil and gas remains robust for decades–and the firm’s models suggest those fuels will supply more than half of the energy mix for another 20 years—the “US energy dominance” focus of the Trump administration becomes challenging over the long term.

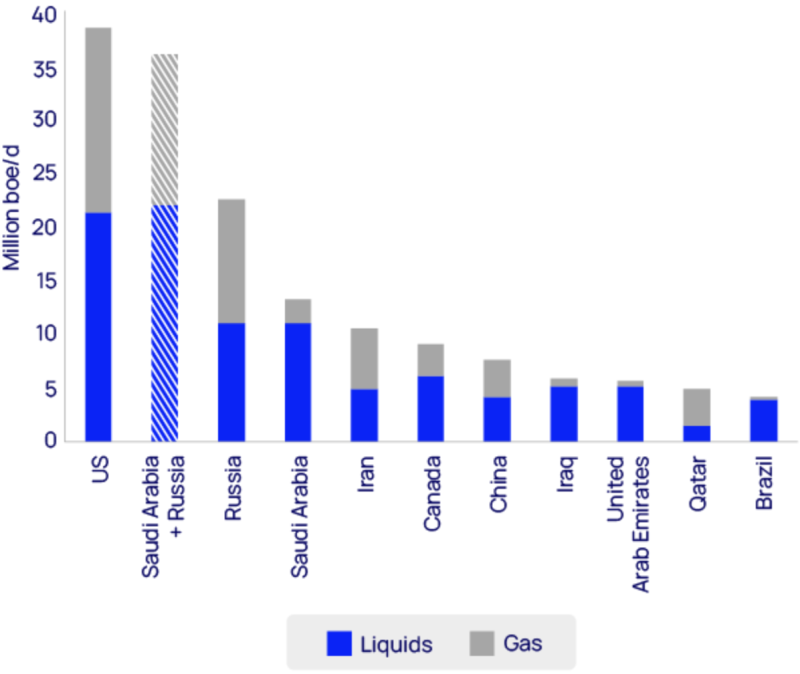

Currently, oil and gas supply 52% of the world’s primary energy, and the US serves as the world’s largest producer of oil and gas. The US, which accounts for 20% of global oil production and 25% of global gas output, produces more hydrocarbons than its two largest competitors combined and last year became the world’s largest exporter of liquified natural gas. US production has risen threefold over the past 15 years, largely thanks to the shale revolution.

"The US has achieved remarkable success in oil and gas production over the past two decades," Robert Clarke, vice president for upstream research at Wood Mackenzie and report coauthor, said in a press release. "Maintaining this dominance will require addressing several key challenges, including resource maturation and an ongoing global shift towards lower-carbon energy sources."

Projected Decline

While the authors see US upstream dominance continuing for some time, US oil and gas production is projected to decline by about 1.7 million BOEPD between 2035 and 2040, even as low-carbon energies continue to expand globally.

Current production in the US is so large, the authors state, that “just offsetting natural declines is challenging” and requires the Lower 48 to add the equivalent of Norway’s production annually just to keep production levels flat. But the shale resource in the US is maturing, and recovery per foot drilled has “turned stagnant in the largest producing reservoirs,” the authors said.

Other factors could affect US dominance, including tariffs and cross-border carbon taxes.

“In Wood Mackenzie’s base-case forecast, US dominance comes under pressure as production volumes—primarily oil—begin to decline in the early 2030s. But if demand expectations erode and a drop towards US$50/bbl emerges for crude, declines would occur much sooner and be more severe,” the report said.

That projected plateau could have far-reaching implications, such as increasing the difficulty in raising capital for big investments, and the possibility that those purchasing US energy exports may step back or slow down volumes, the authors note. Finally, while the US sector has been configured to optimize drilling and completions when prices are high, it has less expertise in enhancing value from late-life production and declining assets, the report said.

Continuing Dominance

It’s important for the US oil industry to look to its strengths to preserve or extend its global dominance, the report said. Those strengths include shale innovation, exploration, and fiscal terms.

“Additional shale innovation can lower supply costs. Refreshed exploration can help offset overreliance on producing assets. And making the country’s unique upstream fiscal framework even more attractive can help pull in more capital.”

Technology innovation, better resource recovery, and improved supply chains helped producers drive down breakeven costs for shale developments.

The report’s authors cited ExxonMobil’s pioneering development of subsurface diagnostics and reservoir models as one example of technology initiatives that can lower the cost of supply.

“If new digital tools can lower breakevens by US$5/bbl, which we think is possible, future tight oil projects will remain as competitive as any other global supply source and extend the Permian Basin’s production profile.”

Operators need to explore to replenish inventory, but the sector’s exploration spending is down 65% since 2012, according to the report. WoodMac models suggest the industry will drill nearly half of its remaining low-cost tight-oil locations within the decade.

And where play-opening projects in the Utica, Uinta, and deeper Permian Basin benches have had good results, the industry needs midstream investment to make the opportunities as viable as existing assets, the report said.

Similarly, the authors noted, shale’s early buildout of pipelines was a key enabler of growth although long-haul interstate pipeline expansions have slowed. But improved buildout would help, noting the Trump administration is reforming permitting frameworks to speed infrastructure expansion.

The authors said continued cost reductions and the addition of resources could steady the US’s footing, but if the energy industry ultimately moves toward lower carbon, overreliance on the upstream sector for too long leaves the US exposed.

“Excitement over the US upstream growth story should not mask the reality that the world does not stand still. If the US wants to remain the dominant energy supplier to the world, it cannot sit idle either,” the report said.