US upstream dealmaking is showing clear signs of slowing, according to a year-end report from Enverus Intelligence Research (EIR), which recorded $105 billion in mergers and acquisitions (M&A) for 2024.

While this marks the third-highest annual total the firm has ever recorded in the US sector, EIR noted that the fourth quarter saw just $9.6 billion in deals, marking the fourth straight quarter of declining M&A value.

EIR attributed the slowdown in its 29 January report to a shrinking pool of acquisition targets after years of consolidation in the US shale sector. Companies that have recently completed deals are also focused on integrating their acquisitions rather than returning to the M&A market immediately.

“Increased volatility in oil prices may have also deterred some buyers, while there is rising enthusiasm for gas and gas-weighted assets to feed burgeoning demand from [liquefied natural gas (LNG)] and data centers,” Andrew Dittmar, principal analyst at EIR, said in a statement.

Austin, Texas-based EIR reported that gas-focused deals totaled $20 billion last year, a fourfold increase from 2023.

The largest deal announced in the quarter was Coterra’s $3.95 billion acquisition of privately held oil producers Avant Natural Resources and Franklin Mountain Energy. The combined transaction pushed the Permian Basin’s share of fourth-quarter M&A to more than 40%.

EIR forecasts continued interest in the Permian but notes that Coterra’s acquisitions have left fewer opportunities in the region's Delaware Basin. In contrast, the Midland Basin likely offers more private operators that are eager to exit.

“For buyers considering acquiring one of the remaining Permian targets, the question will be if the quality and resource expansion upside is worth the price of admission. For many companies, particularly smaller-sized [explorers and producers] that have modest valuations on their own stock, the decision is likely to be to look elsewhere,” added Dittmar.

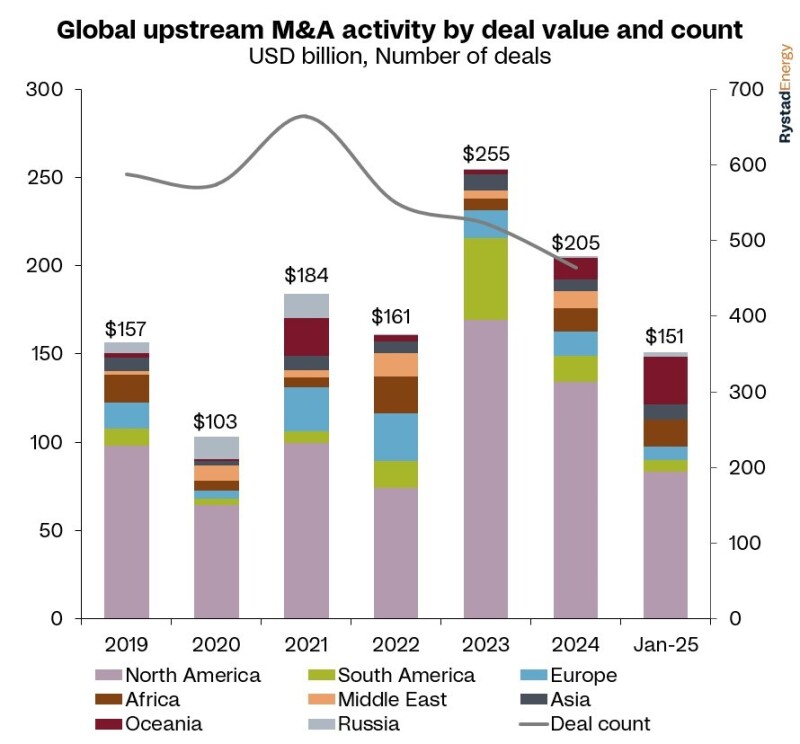

A separate research note from Rystad Energy published 3 February highlighted that the ongoing slowdown in US upstream dealmaking comes after 2 years of record-high transaction values. The Norwegian consultancy said this signals that much of the US shale sector’s consolidation has played out, making a return to those highs unlikely.

With US M&A activity cooling, Rystad estimates the global pipeline for deals stands at around $150 billion, with $80 billion in potential buying opportunities still available in North America.

“Activity was always expected to fall after such dramatic highs, but there is still plenty of business to be done. North America is still a leader in M&A activity and will continue to play a key role in maintaining the market's health. There is also potential for further upside if US shale gas M&A activity increases, assuming Henry Hub prices remain stable and conducive to dealmaking." Atul Raina, vice president of oil and gas research for Rystad Energy, said in a statement.

Rystad also said the Middle East is poised for M&A growth after recording nearly $9.65 billion in transactions last year, the region's second-highest level in the past 5 years. LNG expansion projects and national oil company-led megaprojects are driving renewed dealmaking in the region.

Rystad said key projects include QatarEnergy’s expansion of its North Field to boost LNG output to 142 mtpa by the early 2030s. Analysts are also watching reports suggesting ADNOC may award an additional 5% stake in its Ruwais LNG project to an international partner. Despite the strong outlook, Rystad cautioned that geopolitical tensions in the Middle East could deter some buyers and slow deal activity.

In Europe, upstream M&A activity fell 10% last year to $14 billion. The largest deal saw Shell and Equinor merge their UK North Sea portfolios, creating the region’s top producer at 140,000 BOE/D. While $8 billion in assets remain on the market, tighter UK fiscal challenges could weigh on future deals in the region, Rystad said.