Despite a plateauing of rig count growth in the latter half of 2017, Westwood Global Energy Group is projecting multiple years of double-digit growth in activity and expenditure for the US onshore drilling and completion market. Westwood recently made this projection in its US Drilling & Completion Market Forecast Q1 2018, a basin-by-basin outlook using data gathered by the Energent Group, a market research firm recently acquired by Westwood that is focused on well life cycle and frac market intelligence.

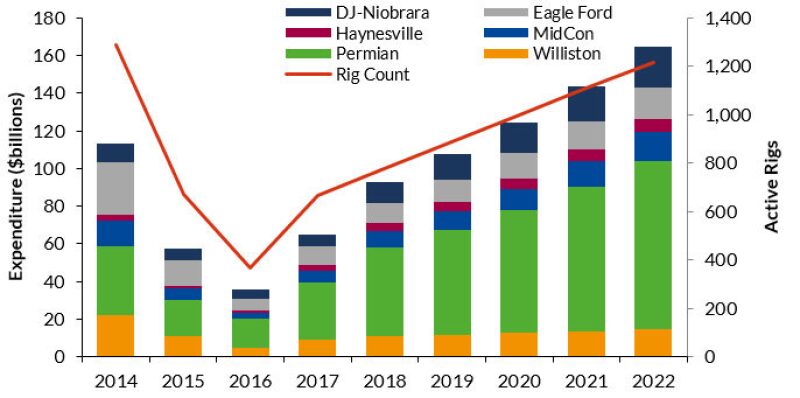

The report said that 2017 represented a marked recovery in activity and expenditure across the six basins covered in the report—DJ-Niobrara, Eagle Ford, Haynesville, Mid-Continent, Permian, and Williston—and through the wider US onshore sector. An 82% increase in expenditure last year was highlighted alongside a 60% increase in drilling and a 28% increase in completion activity. Well designs have also increased in complexity, with a continuation of trends to longer laterals, and an increasing number of stages pushing up per well costs in order to maximize recovery per dollar spent.

Westwood expects this recovery to continue over the length of its forecast, with total rig count rising above 1,000 by the end of the decade. However, the report argues that a more important development will be the relaxation of supply chain constraints as service providers increase their frac sand and spread capacity in 2018. This will allow completion activity to accelerate, resulting in a projected 54% increase in completion spend this year.

The report also projected that $63 billion will be spent across the basins covered from 2018 to 2022, and this expenditure will grow ahead of the rig count as a function of service pricing increases and increasing oilfield services intensity per well. Westwood expects 15% total expenditure compound annual growth rate. Completions are forecast to account for 69% of total expenditure over the period, with the Permian dominating both spend (the report projects 53% of total spend to come from the area) and activity (49% of well spuds).

The rig count for the six basins is likely to reach 1,216 in 2022, an 83% increase from the 2017 average. Upside is projected at $93 billion in the high oil price scenario and $56 billion downside under the low price scenario. These figures are based on an assessment of future oil prices that sees a gradual upward increase within the $55–65/bbl range through the end of the decade, before climbing to $68/bbl in 2022.

The basins covered in the report saw a significant uptick in activity following oil prices rallying in mid-2016. Westwood said that continuing recovery through 2017 has led to rising prices across the supply chain, as spare capacity has been reduced and both drilling and completion crews have been in short supply. Based on an expectation of rising consensus commodity prices to 2022, the US market is expected to enter a period of sustained growth in activity and spend.