US natural gas production has grown rapidly over the past decade thanks to the shale revolution, but lower gas prices and strict financial discipline from operators are expected to ease the momentum in 2020.

A report from data analytics firm Enverus projects US dry gas output growth to shrink to 2 Bcf/D next year from 8–9 Bcf/D in 2018 and 2019, based on early guidance by operators and assuming commodity prices of $55/bbl for West Texas Intermediate crude oil and $2.50/MMBtu for Henry Hub gas.

“There is also downside risk on this forecast, which is most likely expected to get reduced once guidance is finalized in the next couple of months,” Enverus said.

The report notes that weaker gas prices at the end of 2019 and operator emphasis on free cash flow, debt reduction, and shareholder returns are driving capital expenditures lower in 2020, with gas-weighted producers averaging a 25% capex reduction.

Two of the larger US gas producers, EQT and Chesapeake Energy, have reduced their budgets the most on an absolute basis, together shedding $1.1 billion. Six Appalachia pure-play operators—EQT, Cabot Oil & Gas, Southwestern Energy, Antero Resources, CNX Resources, and Montage Resources—have collectively cut their budgets by $1.5 billion.

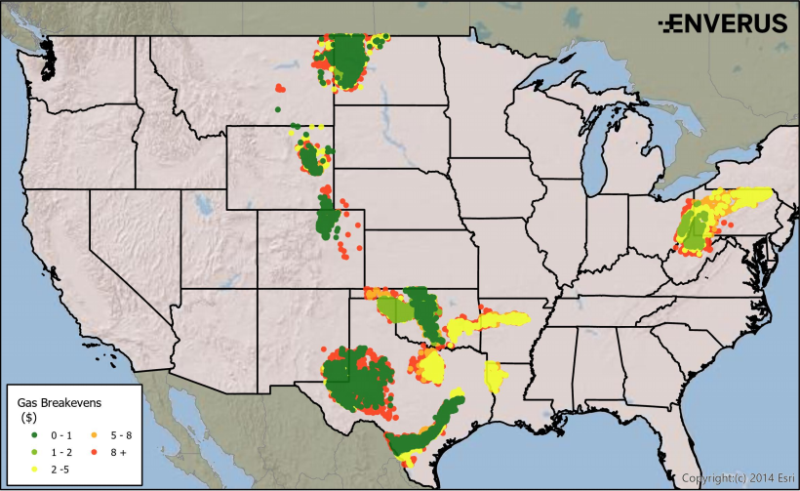

In addition, Chevron said on 10 December that it will reduce funding for its gas projects after taking a $10 billion–$11 billion impairment charge, with more than half coming from its Appalachia Shale assets.

Appalachia will likely close out 2019 having added about 1.7 Bcf/D from December 2018 to December 2019. Looking ahead, Enverus said, the region is expected to continue to struggle with capacity constraints, especially during low-demand periods.

In the Permian Basin, where an excess of associated gas has caused a problem with excess flaring, promising basin economics will continue to face takeaway capacity constraints. Some relief was provided in 2019 via the startup of Kinder Morgan’s 2-Bcf/D Gulf Coast Express pipeline, but it was quickly filled to capacity.

While the Haynesville Shale has yielded more than 1 Bcf/D of year-over-year growth, much of it has likely come via Tier 1 acreage—the only area in the play to offer decent value at a $2.13/MMBtu gas breakeven, Enverus said.

Meanwhile, domestic demand is seen growing slowly over normal weather scenarios with upside risks in colder winters. In 2020, Enverus expects demand in the US to average 77.2 Bcf/D, up 0.3 Bcf/D compared with 2019. It expects gas inventories to end the season at 1.7-2.0 Tcf, weighing on prices next year.

“In 2019, natural gas demand in the US averaged only 6% higher than normal,” said Rob McBride, Enverus senior director of strategy and analytics. “Add to that pipeline constraints and clear signals from operators they’re at a breaking point, and the writing on the wall becomes pretty clear—we’re expecting a significant slowdown in the growth of US natural gas production next year.”