Small to mid-cap oil and gas companies will continue to explore and develop new fields, particularly in South America and West Africa, as the industry bounces back in the next 12 to 24 months; and there will be plenty of investment capital to finance the activity.

Gas will be the focus as companies evolve their portfolios and business models to accommodate the inevitable decline of oil and coal and the rise of lower-carbon fuels.

Those are just some of the findings in the London-based Energy Council’s 2021 Future Outlook Survey Report published in March and based on a survey of the Council’s membership of 100,000 senior energy executives.

The Energy Council is a networking platform that facilitates dialogue between decision makers in energy companies and the finance and investment communities. Nearly half of the responses to the January 2021 survey (48%) came from North America and Europe, while 28%, the second-largest grouping, represents opinion from Africa or Asia.

Oil and gas company executives and consultancies, including law firms, comprised 60% of the respondents—37% from upstream companies and 22% from the consulting side.

In reporting their findings, the Council noted that “the survey highlighted that there is still an appetite to invest in, and finance, oil and gas projects; according to over 60% of our participants, there is capital available for those who want it, RBL (resource-based lending) is not dead (47%), and there is a future for private equity (82%).”

Moreover, the report stated: “Positive news flow around the vaccine, the gradual decline in US shale production, and the move by OPEC+ to restrain output into mid-2021 have all provided the impetus for WTI to rise firmly into the $50s and stay there according to over 50% of respondents.”

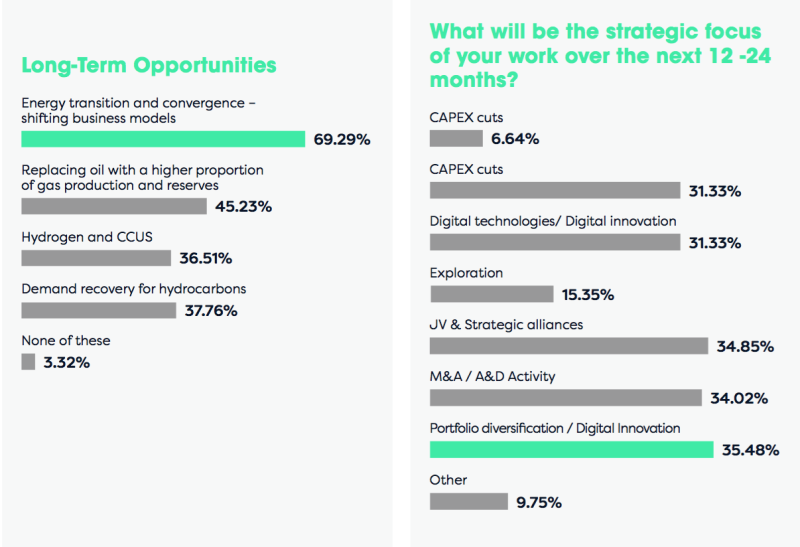

So, with capital available and macroeconomic conditions improving, more than 53% of respondents said that exploration would continue to play a role in their business strategies. Such answers came largely, though, from small to mid-cap respondents; international oil companies predominantly answered “no,” the report noted.

“For those who are still pursuing an exploration strategy, the majority are interested in the potential for West Africa (33%), South East Asia (21%), and South America (34%),” the report stated. “With discoveries in both the MSGBC Basin (Senegal/Mauritania) and Guyana dominating headlines in 2019 and 2020, these results are not unexpected. Suriname is also an area of interest.”

Responses like these suggest a “business as usual” attitude exists on the part of oil and gas decision makers and influencers. However, when it comes to “future-facing” issues such as the low-carbon energy transition and the digital world, things aren’t quite as clear-cut.

For example: “Whilst a majority of companies were preparing to move towards a less carbon-intensive energy mix (55%), and 50% expected to diversify their business outside of oil and gas, 40% of respondents did not have an ESG (environment, social and governance) program in place and 77% were either not planning to implement one or weren’t sure if their organization already had one.”

So not surprisingly, gas surfaced in a big way to metaphorically “kick the can down the road” and buy time to build the new business models, infrastructure, and value chains required to transition from fossil fuels to new, low-carbon sources of energy.

In all, nearly 70% said they would be shifting their current business models, and more than 45% said that shift would be moving in the direction of replacing oil with a higher proportion of gas production and reserves, according to the survey.

More than a third (37%) said they planned to diversify into hydrogen and CCUS (carbon capture utilization and storage), thus confirming the industry’s intention to produce blue hydrogen from gas and thus position gas as the fossil fuel of choice in the green-energy landscape.

As for digital, it is no secret that oil and gas companies have lagged behind other industries in fully embracing the global digital transformation.

And not surprisingly, the Energy Council found that the human factor plays the biggest role. According to the report, 46% of respondents identified “company culture as the biggest barrier to implementation” of “new digital technologies into their work flow and workforce,” and that a lack of investment (34%) in digital is directly related to a hesitancy to spend money on technologies that evolve so quickly they become outdated almost as quickly as they are implemented.

Recent International Energy Agency research shows total demand to increase and slightly exceed 2019 levels by as soon as 2022. The survey showed that almost half of respondents have no plans to increase CAPEX in the next 12 months.