The US onshore operator that eventually thrives in the 2020s may now look something like Chesapeake Energy or Samson Resources II. It also might be backed by Quantum Energy Partners.

The chief executive officers of those firms—two of which helped usher in the unconventional revolution—outlined their roles in an industrywide transformation at the NAPE Global Business Conference in Houston this week. Recent news of wheeling and dealing by operators added color to an event populated by leaders determined to prepare their companies for a new era in the upstream space.

Much discussed by speakers and attendees were several deals announced in just the past week following a relatively slow last three quarters of acquisition and divestiture activity. Among them were Chesapeake divesting part of its Midcontinent position, WPX Energy exiting the San Juan Basin, ConocoPhillips buying Anadarko’s nonoperated interest in Alaska’s western North Slope, and Halcon Resources expanding its Permian leasehold.

Of particular note was the proposed merger of Midstates Petroleum and SandRidge Energy, whose previous merger agreement with Bonanza Creek Energy last year was struck down after a protest led by activist investor Carl Icahn, who once upon a time pushed for big changes as a major Chesapeake shareholder.

Those deals represent an ongoing trend since the downturn of exploration and production (E&P) companies consolidating their operations, specializing in just a few regions, de-levering, and professing their allegiance to cash flow neutrality. But, in the cases of Chesapeake and Samson, their problems were glaring even before commodity prices sank.

Reimagining a Shale Pioneer

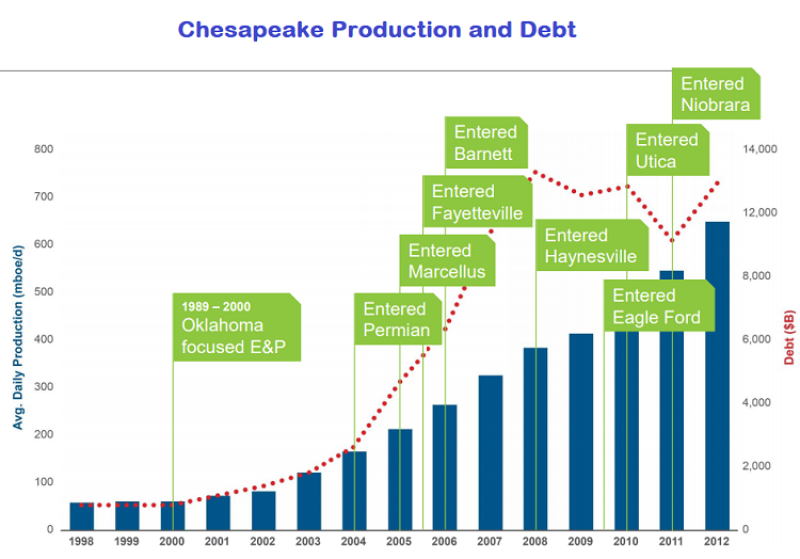

Doug Lawler, Chesapeake president and CEO, explained during a luncheon just how bloated his company had become amid the unconventional boom and high oil prices. When he took over the Oklahoma City independent in 2013, it had 11 million net acres across the US, was the No. 2 most active driller in the country, and was the No. 1 driller of horizontal shale wells in the world, he said. At its peak, the company had a rig count of 180, more than double any other US operator. The company was focused on volume and activity with 23 consecutive years of growth.

Founded in 1989, Chesapeake started as a company with principal operations in Oklahoma but, beginning in the mid-2000s, began a large-scale expansion into almost every major unconventional US basin—the Permian, Marcellus, Fayetteville, Barnett, Haynesville, Eagle Ford, Utica, and Niobrara—leading to a debt load of $13 billion at the end of 2012. The company was spending $15 billion/year and making just $5 billion/year.

Meanwhile, organizational complexity had sprawled out of control. While the company had interests in more than 45,000 wells, production of 700,000 BOE/D, and an employee headcount of 12,000, it also was involved in numerous other ventures that had nothing to do with the industry, including investments in businesses such as restaurants.

“We had a huge enterprise, a significant asset base, and a very strong and talented employee set, but frankly, at that time, the challenges were now too big for the organization and resulted in activism” from Icahn, a then-shareholder who pushed for major change. In addition to high debt, poor capital efficiency, and low margins, Lawler had to contend with excessive production and general and administrative (G&A) expenses and high transportation costs.

Chesapeake had to reassess its core values and determine a new way forward, Lawler said. This included keeping exploration as part of its strategy, though it would have to be funded a slower level than before. “In a low prices environment, when we turn our back on technical excellence–turn our back on exploration—is when the industry has made some of the biggest mistakes.”

While capex has been slashed dramatically since 2012, the company has managed to keep production flat, which Lawler attributes to removing almost $800 million/year in production expenses and cutting G&A expenses in half over the period. At “about one seventh of what was spent 4-5 years ago, we’re delivering the same amount of production for our shareholders as we did back in 2012,” Lawler said.

He said the company has now reduced its debt by a little more than $11 billion in 4-5 years, eliminating $6.7 billion in midstream obligations and $3.2 of near-term debt maturities. It hopes to kill its remaining debt “as soon and as quickly as we possibly can” to target free cash flow neutrality, which could occur as soon as this year, Lawler said.

Helping further that goal is this week’s announcement that the company has signed $500 million in sales agreements for properties in the Midcontinent, which includes its exit from the Mississippian Lime play of the northern Anadarko Basin. The three deals consist of 238,000 net acres, 3,000 wells currently producing 23,000 BOE/D—of which 25% is oil—net to Chesapeake, and related property, plant, and equipment in central and western Oklahoma and the Mississippian Lime. It was separately reported last week that Chesapeake will cut its workforce by 13%, further trimming a headcount that had been down to around 3,250.

The company also has netted about $80 million from the initial public offering of FTS International, a large well completions company in which Chesapeake owns a 30% stake. Chesapeake held on to 22 million shares.

After around $3 billion in asset sales by Chesapeake over the last few years, it now has six asset bases in the US comprising 5 million acres, of which 60% is undeveloped. Three—the Marcellus, Utica, and Hayneville—bolster the company’s gas production, which represents 4.5 Bcf/D and is capable of flowing 7 Bcf/D. With positions in the Eagle Ford, Midcontinent, and Powder River Basin (PRB), the company’s overall oil output by yearend 2017 exceeded 100,000 B/D, a number on which the company plans to continue building, especially with the possible emergence of the PRB as a major oil play.

Shifting From Old Guard to New School

Predating Chesapeake by 18 years, Tulsa-based Samson Resources’ reinvention is built around its oil-heavy stake in the PRB, a big shift from its history as a gas-heavy producer spread across several basins, including a longstanding focus on Oklahoma, East Texas, and North Louisiana

Joseph A. Mills, president and CEO of the aptly-named Samson Resources II since its emergence from bankruptcy in March 2017, kicked off a slate of speakers on Feb. 7 by outlining the anatomy of a restructuring. The evolution of Samson captured some of the same themes involved in the Chesapeake story but came from the perspective of a smaller, more brittle operator.

Previously family-owned, the company was once one of the largest privately-held E&P companies in the country. When it was purchased by private equity firm KKR in 2011 for $7.1 billion, it boasted more than 2 million net acres, 11,000 gross wells, 700 MMcf/D of gas equivalent production, and more than 1,200 employees. Its diverse range of assets were in the Midcontinent region, East Texas and North Louisiana, the Permian, the Rockies, the Bakken, and the Marcellus. At the time of the deal, gas prices were slightly higher and the company was heavily levered, Mills said.

A divestment program began almost immediately in 2012 and lasted through the downturn, leading up to its eventual bankruptcy filing in 2015. “It was a pretty acrimonious bankruptcy,” Mills said. “We were the second-longest energy bankruptcy, only behind TXU Energy, which went on about 4 years. Ours was close to 18 months. So it was a challenging time, certainly with the unsecured creditors unhappy. Everybody was unhappy.”

A group of hedge funds from New York City bought a large portion of the second lien “for pennies on the dollar, and they really took control of the bankruptcy, and quite frankly I give them all the credit,” he said. “There was a period of time there, probably in December of 2016, when it looked like the company was going to go Chapter 7. It was that challenged and there was that much acrimony.”

When Samson emerged, it had eliminated more than $4 billion debt and had stuck with three core assets—East Texas and North Louisiana, the PRB, and the Green River Basin (GRB)—had a total of 490,000 acres, and produced 135 MMcf/D, of which 75% was from East Texas. It also had just 250 employees, down by almost 1,000 from a few years earlier.

However, the company still had the G&A expenses of a company 10 times its size, Mills said. It remained “highly levered” with a borrowing base of $280 million, of which $245 million was drawn. “We probably had $25 million in liquidity,” he said, and the company was still heavily gas weighted with no hedges in place. “So we were wildly exposed to the commodity prices cycle at that point.” Previously a self-described bull on gas, Mills believes “gas prices are going to be challenged quite frankly for a long time.” When it came to hedging, “if there was a [$]3 in front of it, I took it all day long.”

|

“There was a period of time there, probably in December of 2016, when it looked like the company was going to go Chapter 7. It was that challenged and there was that much acrimony.” —Joseph A. Mills, president and CEO of Samson Resources II |

A strategic review indicated Samson’s best assets were in the Rockies as opposed to the shale gas producing Haynesville, where wells were too pricey given the company’s lack of cash. Meanwhile, there was “a real strong appetite for Haynesville production and development activity,” he said. Mills believed “the days of being a diversified, large company were over” and “felt really strongly that we needed to reposition the company strategically.”

Samson sold its East Texas and North Louisiana assets for $525 million in cash to Rockcliff Energy II, whose outside investor group is led by Quantum. It also sold some of its Midcontinent assets. “All in, we raised about $550 million in 4 months after emerging,” he said. “The next thing we did is hedge, hedge, hedge.”

Within 7 months of emergence, it had paid off all of its debt. “We really are much more of a startup today,” Mills said, adding that the company is so lean that it outsources its accounting and human resources work. While it is technically a private company, it almost acts as a public one to cater to its 125 equity owners mostly consisting of big banks and New York City hedge funds.

Now a pure-play Wyoming-focused company that’s weighted 70-80% toward oil, Samson has 200,000 net acres in the PRB and GRB, of which 150,000 are in the PRB, making the company the 6th largest land owner in a region where it is rubbing shoulders with Chesapeake, Devon, Anadarko Petroleum, and EOG Resources. Samson has identified 1,370 net drilling locations, heavily weighted toward the PRB, representing “years and years of drilling opportunities ahead of us,” he said.

With its work ahead cut out for it, Samson expects to spend $130-150 million this year, more than the firm initially reported, and drill 15-20 net wells. It plans to grow oil production by close to 20%, while it is 90% hedged in oil and 100% hedged in gas, “which kind of gives us an insurance policy,” Mills said. The company now has a “strong balance sheet” with about $100 million in cash and $100 million undrawn from its revolving credit facility.

Mills remains mindful that Samson’s investors are hedge funds that want to see returns. “When they hired me, honestly, it was to sell the company as fast as I could,” he said. But he added that its returns thus far have “extended the runway a little bit.”

Fueling the Transformation

Rockcliff Energy is just one of 20 companies Quantum currently backs in the E&P space. “If you were to aggregate all the companies we have investments in today, we’d look really similar to a superindependent,” with 2.3 million net acres, 350,000 BOE/D, and 32 rigs working across the US and Canada, said Wil VanLoh, Quantum founder and CEO.

The 20-year-old, energy-only firm directs 75% of its capital to upstream and has backed 90 companies. It currently manages $15 billion in capital and just finished raising $5.25 billion as part of its Fund VII—for which VanLoh was seeking investments at NAPE.

Noting Quantum’s in-house technical capabilities, he recounted a 2012 deal in which the firm bought an asset from Chesapeake for $500 million that turned out to be in the SCOOP play. The firm spent more than $1 billion to develop the properties and then sold them a few years later for multiple times the purchase price despite strip prices falling 30% since the deal. VanLoh credited his team for driving down drilling and completion costs per lateral foot by 50% while boosting recoveries.

“Some of the largest success stories that we hear about in the public realm today started as private companies,” noted VanLoh. Outside the Permian and Appalachia, more than 25% of rigs working in every basin are run by private equity companies, he said. “Probably 60-70% of the rigs running in the US today are running with assets that are currently in private equity hands or at one time were in private equity hands.”

|

“If you were to aggregate all the companies we have investments in today, we’d look really similar to a superindependent.” —Wil VanLoh, founder and CEO of Quantum Energy Partners |

He emphasized that unconventional oil and gas changed the scale and capital intensity of the industry. A decade ago, it took around $16 million to develop a section of eight wells, and now the same section of land requires north of $250 million, he said. “We used to get maybe a million barrels out of a section of land. Today, that number can be 20, 25, 30-plus million BBL depending on the number of zones.”

Public markets responded in full force to the increasing need for capital, but private equity funds also multiplied. “Since 2010, we’ve had over $200 billion of fresh, private capital raised by private equity funds active in the space. And that’s also grown the number of companies that are receiving that capital. By our count today, we’ve got 366 privately-backed companies that we track” active across North America, though more than half are active in just the Permian and Midcontinent, he said. “So, if you’re going to start a new company today, it might make sense to look somewhere other than those two regions.”

Based on current opportunities in resource plays that are economic to develop at current commodity prices, there is more than $6 trillion of drilling and completion capital that can be spent today, VanLoh said. Canada and infrastructure add another $3 trillion. “What’s not in short supply is opportunity. What is in short supply is great managing teams to go and exploit that opportunity,” which is where private equity can swoop in and provide support.

“There’s a huge focus today on living within cash flow,” VanLoh said. Public markets feel like they were too generous for a long time. Those living within cash flow and growing production are being rewarded with better multiples. Those who can’t are being hurt. Meanwhile, private equity continues to expand its offerings to keep pace in a changing industry, including providing growth capital, re-caps, partnerships with public companies, and even selling to other private equity sponsors, something previously seen as taboo. Going forward, it will have to focus on scaling up its companies, which “will require more people, more capital, and more time.”