Liquefied natural gas (LNG) has been in global energy supply discussions for decades. Geopolitical tensions, however, recently elevated it from a bullet point to the entire conversation.

Rarely does a day pass without mention of signed long-term LNG purchase agreements or LNG terminal construction projects advancing, one day making it possible to transport the curiously cold molecules across oceans to eventually power industries or heat homes.

So strong are the fundamentals of the LNG industry, for example, that they were cited as a primary driver in the conversion of one of the largest pure-play US-listed shipping companies—Capital Product Partners led by Greek shipowner Evangelos Marinakis—to a pure-play LNG shipping company.

In addition to changing its name to Capital New Energy Carriers, the partnership is selling off its modern fleet of 15 Neo-Panamax and Panamax container vessels.

It will spend $3.13 billion to purchase 11 newbuild LNG carriers (LNGC). According to an announcement on 13 November, the first of the new vessels arrived in October 2023. The company already had seven LNG carriers in its fleet, with the remaining 10 newbuild vessels scheduled for delivery through March 2027.

Jerry Kalogiratos, chief executive of Capital Product Partners, said the acquisition was transformative, noting that the partnership “expects our contracted revenues to increase by 87% percent to $3.1 billion, our revenue weighted charter duration to 7.2 years as of the closing date, and the average age of our LNG fleet to decrease to 3.2 years by the time all LNGCs have been delivered in 2027.”

LNG Market Overview

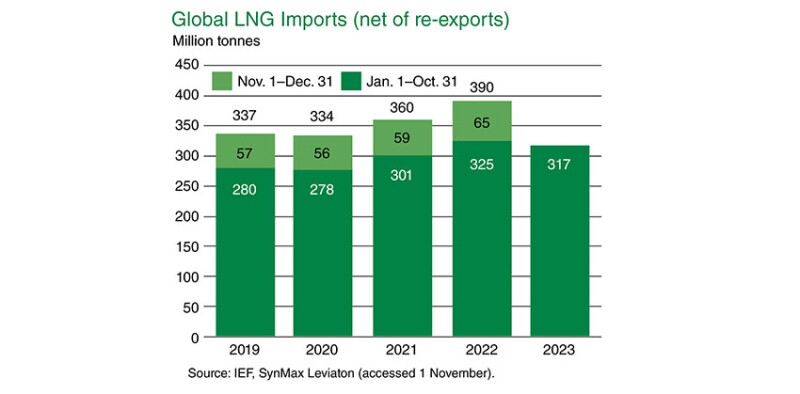

Events like the Russian invasion of Ukraine in February 2022 and the sudden loss of Russian pipeline gas supplies upended global energy markets. European buyers turned to LNG imports to meet demand. According to Wood Mackenzie, the current conflict in Israel/Gaza, possible pipeline sabotage in the Baltics, and the threat of fresh strike action at Australian LNG facilities all pushed spot prices up 35% through October.

In a November blog post, Wood Mackenzie noted that a record 200 mtpa of new supply is under construction as “players bet big on Asia’s push to reduce its dependence on coal and Europe’s need to replace Russian gas.”

While the proliferation of LNG projects is prompting concerns that there may be too much LNG on the market once these projects are completed, this is not the case, according to Wood Mackenzie.

“Increased supply availability will bring prices down and boost demand growth,” said Gavin Thompson, vice chair of Europe, Middle East, and Africa, and Massimo Di Odoardo, vice president, gas and LNG research for Wood Mackenzie, noting that the market will need another 60 mtpa of new LNG by 2033.

“Much will hinge on sustained economic growth, driving increased demand across emerging markets in Asia.