As the world reaches a tipping point in its will to address climate change, the industry must find a new way forward, especially in the United States.

Many are right to say that oil and gas are not going away; the transition is planned to take 30 years or more and will not decline to zero production. This fact, though, obscures the reality that peaking, then declining, demand for oil—gas is another story—will structurally change and globally redistribute the industry’s exploration and employment.

The story of oil supply and demand began its race to the top 150 years ago. “Shortage” and “glut” have meant that paired growth got out of sync, not that there was a real loss of production. For many decades the world has needed about 1 million B/D more each year than the previous year, but on a percentage basis growth has slowed. At the same time supply from previous years declines about 5 to 6% per year, arguably higher in recent years. The treadmill for new supply has been running hot for decades.

All major public forecasts in the past year call for oil demand to plateau between now and about 2030 when accounting for ongoing changes to policy. (To be clear, some show a peak in the 2030s in “business as usual” cases, but they also show even sooner peaks if policy and demand changes accelerate). BP’s Energy Outlook 2020 from last fall took the bold—and well-argued—position that peak oil demand is today and that it is only a question of how fast demand declines. “Peak” demand isn’t really a peak like the Matterhorn; it is flatter like a weathered jebel. We know this from the example of the peak oil demand experienced by the developed world. We also know from that experience that forecasting agencies failed to predict the peak OECD oil demand in 2005 literally by decades even as demand turned down.

Reversal of demand growth presents a figurative and mathematical inflection point. Though existing production continues, growth becomes negative, and the pace of the new-supply treadmill plummets. When the need for new supply approximately halves, the Pareto principle tells us that the number of new projects required will fall more than half. Thus, the need for those industry professionals preferentially tasked with finding new oil supply—geophysicists, exploration geologists, drillers, reservoir engineers, landmen—may fall quickly. Other disciplines like operations that service existing production will face only the headwinds of cost reductions and then the long, slow slide toward mid-century targets.

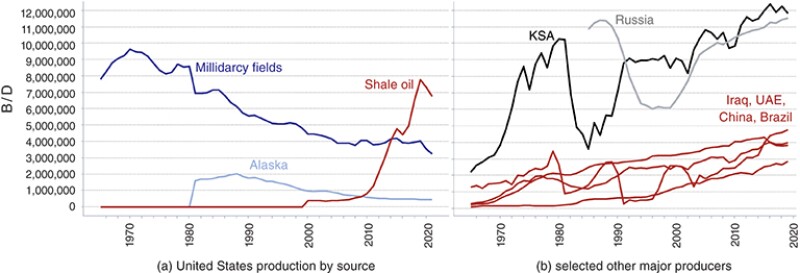

The United States via its swarm of large and small companies has dominated the global supply story for more than a decade with its unique shale revolution, but it had previously shriveled to a second-tier producer. Fig. 1 shows 55 years of oil production history. Fig. 1a shows the US supply deconstructed to its functional parts while Fig. 1b shows ascendent producers on the same scales.

Hubbert’s theory of creaming discoveries and peaking production has proven correct. US “conventional” production from millidarcy fields peaked 50 years ago, before I was born. North America got an early start into his curve, exploration progressed through about three dozen basins over more than a century, and the country crested early. Now the activity and the size of new millidarcy discoveries in the US lies deep in secular decline.

Despite Herculean policy efforts in the 1970s and 1980s to increase domestic sources, production only modestly reversed (but did set up the shale revolution). Activity steadily concentrated in major basins, and producers reduced headcount to focus on cost-efficient operations. In the early 2000s, vertical drilling ramped up with a second titanic effort due to extraordinary commodity prices, but the production decline did not abate at all this time. Following the 2008–2009 upheaval, vertical drilling held at about half of its previous rate, and there was a small resurgence of drilling in secondary basins. That drilling was already falling off when the 2015 crisis plummeted vertical drilling by about three-quarters. Vertical new drills have become a tiny fraction of their historical counts, and I see no signs of renewed interest in exploration or development for millidarcy fields coming out of this latest cycle. Investment interest also wanes as professionals with relevant experience retire.

The US re-emerged as a global producer riding a wave of reckless and commonly unprofitable shale development, but there have been no new shale plays discovered in the US for at least 6 years. On average, shale producers are now drilling lower-quality geology than in previous years. Initial rates have been increasing, but so have initial declines. Last year’s pause in drilling surfaced the inherent natural decline as US supply dropped 15% in just a few months. Public forecasts of future US shale production demonstrate a consensus that shale production continues declining from here.

In short, the geology of North America is extremely picked over. The best opportunities to meet future demand reside in other parts of the world. For simple comparison, see Fig. 1b which shows how other dominant producers, especially Russia and the Kingdom of Saudi Arabia (KSA), have grown production continuously except for short periods of major political disruptions. Even when millidarcy production peaks, those producers have the opportunity to leverage the lessons of the US shale revolution to develop their own source rocks more orderly and profitably. Though figures may be inexact, it is indisputable that KSA and much of OPEC have and will continue to have much lower finding and developing costs plus much lower production costs, both a direct function of less mature geology, and both placing them in the lead in a world of lower prices and less new supply.

In the past, the KSA in particular suffered a handicap in cost competition from its high social costs. There was a time when it required $80/bbl oil or more to meet its obligations to its citizens, but that breakeven cost has been declining since the last price downturn. Its 2021 budget is estimated to require a breakeven price of Brent in the low $50s, translating to a WTI price in the high $40s.

Even when it comes to the environmental issues increasingly valued by users, the US is no longer a leader. It may have historically led the way in protections of workers, water, and land, but today’s battleground floats in the air. The US has about as many idle, unplugged wells as producers, and the average producer is 35 years old. Led by Texas, the US has also come back to the top of the list of most-flaring nations. Between aging infrastructure, low-rate/cost-conscious vertical production, and recalcitrant politics, the US seems to fall in the worst-emitting third of global producers. For these reasons Texas missed out on an 11-figure international gas sales contract late last year.

To be clear, opportunities still exist in the US, and profitable millidarcy wells will still be drilled. Many North American producers are already beginning to shift to strategies focused on highly efficient, technologically leveraged production at scale with demonstrable ESG (environmental, social, and corporate governance) bona fides. Opportunities for new supply still lie in complex, poorly understood reservoirs, particularly uphole of shale plays which have provided a gratis and pervasive view of shallower geology.

The petroleum industry of today also has many of the skills for the sustainable energy industry revolution of tomorrow. As T. Boone Pickens used to say, the US is the Saudi Arabia of wind, and our industry has experience with leasing land, with large and rural construction projects, with maintaining large equipment. It has been estimated that a zero-carbon world in 2050 may require injecting as much CO2 volume each day as we currently produce as oil. Our industry has the unique information, the know-how, and the depleted fields to capture and to store carbon. We have the assets and rudimentary science to create hydrogen in fire floods, and no other industry comes close to serving the many varieties of geothermal energy.

Oil is not going away, but many jobs will simply evaporate—especially in mature and high-cost countries—as exploration falls and finishes its shift abroad and as domestic strategies shift from drilling to cost-efficient production. Some producers and employees will lean into new strategies to ride it down, and some will buy time by side-stepping to natural gas for a while. Still, some companies and individuals will endure the rough launch to ride the rocket trajectory toward a sustainable future.

Dwayne Purvis, P.E. is a reservoir consultant, writer/speaker and trainer based in Texas. He assists operators and investors to make circumspect decisions, especially in hard-to-understand reservoirs and complex situations. Over 25 years of practice and multiple leadership roles, Purvis has studied scores of fields and advised clients of all sizes. He graduated from Texas A&M University and is a member of AAPG, SEG, SPEE, and a 25-year member of SPE. He can be reached at dpurvis@dpurvisPE.com.