Does the world really want carbon capture, utilization, and storage (CCUS)? The answer is an unequivocal “Yes,” say the International Energy Agency (IEA), the Intergovernmental Panel on Climate Change, the United Nations, and many oil and gas companies, among others. The consensus is that rapid scale-up of CCUS is essential for meeting climate and emissions targets while not crippling economic growth. As much as 450 million Mt of CO2 could be captured, used, and stored globally with a commercial incentive as low as $40/Mt, according to the IEA. Yet this potential remains largely untapped.

“It’s a chicken-and-egg problem,” said Dan Cole, vice president of commercial development and governmental relations at Denbury Resources. “To address the challenges, more projects need to be built, but more aren’t being built,” said Cole.

The reasons are many. The engineering sector is trying to scale up relatively immature technologies outside of niche projects and experiencing growing pains. Uncertainty around policy and return on investment (ROI), or lack thereof, is pushing back or halting large-scale projects. Public sentiment is pushing ever harder against carbon of any type in favor of renewable energy.

CCUS encompasses four interrelated areas, each of which face its own distinct technological, financial, and perceptual challenges.

- Capture

- Transportation

- Storage

- Use/Reuse

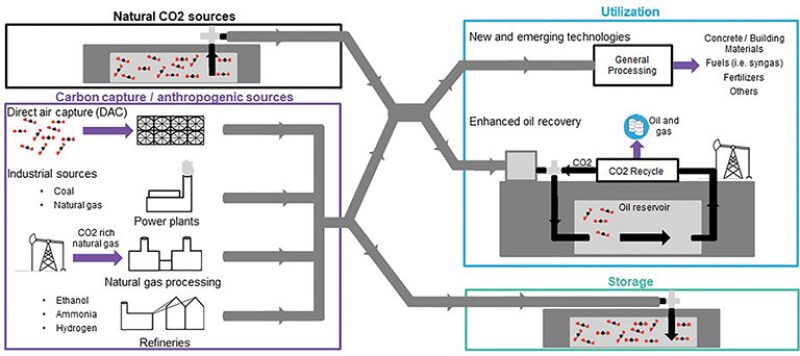

Fig. 1 illustrates the CCUS process.

Carbon Capture—the Least Mature Area

Approximately two-thirds of the total cost of CCUS is attributed to carbon capture. Additionally, capturing and compressing CO2 is estimated to increase the cost per watt-hour of energy produced by 21–91% for fossil fuel power plants, and applying the technology to existing plants would be more expensive, especially if they are far from a sequestration site.

Of all the components of the CCUS process, capture is considered the least technologically mature. Belief is widespread that optimizing a CO2 capture process would significantly increase the feasibility of CCUS because transport and storage technologies are more mature.

Capturing CO2 is most effective at point sources such as large fossil fuel or biomass energy facilities, industries with major CO2 emissions, natural gas processing, synthetic fuel plants, and fossil fuel-based hydrogen production plants. CO2 also can be captured directly from the air through direct air capture (DAC) rather than at a point source. Carbon dioxide can be separated out of air or flue gas with absorption, adsorption, or membrane gas separation technologies. Absorption, or carbon scrubbing, with amines is currently the dominant capture technology. Membrane and adsorption technologies are still in the developmental research and pilot plant stages.

Transportation Issues

Captured CO2 is usually transported to suitable storage sites by pipeline, or occasionally, ships. Enhanced oil recovery (EOR) could reuse a substantial volume of industrial CO2 for injection. The largest EOR opportunity is in the Permian Basin. However, the majority of US industrial CO2 is produced on the Texas-Louisiana Gulf Coast and in the middle of the country, and there are currently no dedicated pipelines to get the CO2 to the Permian Basin.

The US currently has over 5,000 miles of CO2 pipeline installed, and it is estimated that approximately 25,000 miles of new dedicated pipeline will be needed to transport the larger source emissions of industrial CO2 to either EOR projects, dedicated storage, or manufacturing reutilization sites, at a cost of greater than $50 billion. Additionally, there are important unanswered questions about pipeline network requirements, economic regulation, utility cost recovery, regulatory classification of CO2 itself, and pipeline safety, according to the US Congressional Research Service. Federal classification of CO2 as both a commodity (by the Bureau of Land Management) and a pollutant (by the Environmental Protection Agency) could create conflict that may need to be addressed not only for the sake of future CCUS implementation, but also to ensure consistency of future CCUS with CO2 pipeline operations today.

Then there is the question of paying for the pipelines. Various incentives and ideas are being discussed to address legal, operational, and commercial barriers of capital investment for the development of additional pipeline infrastructure, according to Cole, but no pipeline will be put in place unless there is guaranteed throughput of product to offset the cost of construction and operation.

Storage Questions

North America has enough storage capacity for more than 900 years’ worth of CO2 at current production rates, according to the National Energy Technology Laboratory (NETL). Geological formations such as depleted oil and gas reservoirs, deep saline aquifers, and coalbed methane formations are currently considered the most promising sequestration sites. Long-term sequestration of CO2 is a relatively new concept, however, making long-term predictions about underground storage security difficult and uncertain.

CO2 storage differs from typical oil and gas recovery projects in the way the reservoir is managed, according to University of Calgary professor and former SPE Distinguished Lecturer Steven Bryant. But, for reservoir engineers armed with technologies that have been proven over many decades, the technological challenges of long-term CO2 sequestration are significantly less than those of building renewable energy to scale. Additionally, says Bryant, engineers and researchers are looking at storage methods that go beyond injecting supercritical CO2 into vacant pore spaces. Some of these methods could lead to income generation for storage. Bryant is active in an IEA group working on technologies and models for monitoring of CO2 storage.

Similar to transportation is the question of who should pay for CO2 storage. Numerous sites have been identified in the US and other countries for long-term storage. But in the US, complications arise from the fact that arrangements to use these sites must satisfy the business and financial needs of the surface (land) owners, who also own the pore space; the mineral owners (who often are not the land owners); and the mineral lessees (the E&P companies). On publicly owned US lands, including offshore, and in Canada and other countries where the minerals belong to the mother country, storage can be much less complicated.

“While this may seem convoluted, we need to remember that when the US laws governing oil and gas development were written, the purpose was to protect the correlative rights of the mineral owner and for the purpose of extracting the hydrocarbons,” said Greg Schnacke, executive director of governmental relations for Denbury Resources.

Reuse

The oil and gas industry has been monetizing CO2 for EOR since 1972. Because EOR increases oil production, it provides an economic incentive to producers and currently accounts for the majority of CCUS use. Additional applications for captured CO2 include using it as feedstock for production of clean hydrogen, concrete building materials, fertilizer, soda ash, intermediate polymers and chemicals, urea, carbonated beverages, and pharmaceuticals, among others. Most of these applications are in research or pilot phases with varying economics.

It is possible for CCS, when combined with biomass, to result in net negative emissions. A trial of bio-energy with carbon capture and storage (BECCS) at a wood-fired unit at the Drax power station in the UK started in 2019. If successful, this project could remove a tiny amount of CO2 from the atmosphere.

Current Projects

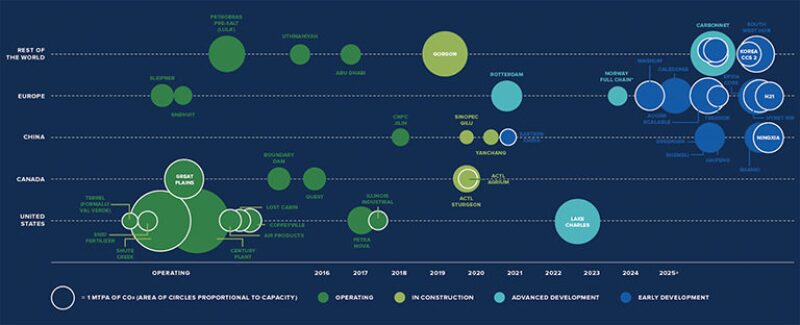

There are currently 23 large-scale CCS facilities in operation or under construction around the world, according to the Global Carbon Capture and Storage Institute (GCCSI), capturing almost 40 Mtpa of CO2. An additional 28 pilot and demonstration-scale facilities in operation or under construction collectively capture another 3+ Mtpa (Fig. 2).

What’s the Holdup?

“The challenges [to CCUS deployment at scale] are significant: the high cost of CO2 capture, lack of infrastructure, absence of policy incentives, and public acceptance,” according to IHS Markit Senior Vice President of Energy and Chief Energy Strategist Atul Arya.

The IEA agrees, saying that for every CCUS project that has successfully reached a final investment decision, at least two large-scale projects have been canceled, citing several factors.

- Long lead times for projects, many of which can take as long as a decade to plan and construct

- The need to reduce the cost of “learning by doing,” which depends on more projects to realize potential and accelerate commercialization

- Lack of confidence in CO2 storage, which requires more work to convert theoretical storage to “bankable” storage

- The need for greater understanding of the future role and availability of CCUS at a local and regional level, to inform today’s energy policy and investment decisions

- Need for more institutional support which includes industry and government as well as the financial and insurance communities

- Lack of community support

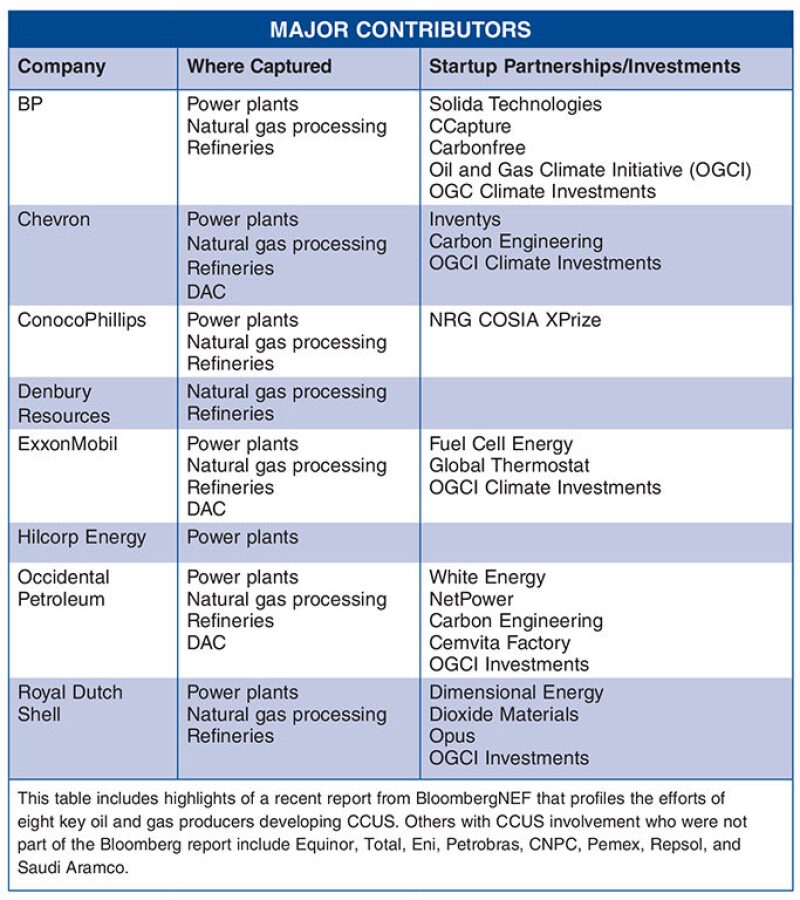

Many experts agree that EOR can’t handle all the industrial CO2 being vented today. Markets beyond EOR are being investigated and pursued, and some are in various stages of commercialization. Several large oil and gas companies are partnering or investing in these opportunities. But, for investment to continue and to become more widespread, investors need assurance for credit durability and long-term certainty, both of which have been lacking until now.

The 45Q Tax Credit—Assistance with Caveats

In 2018, the US enacted legislation that expanded and extended the 45Q tax credit—a US credit program originally enacted in 2008—in a move that, according to the IEA, could trigger new capital investments of $1 billion for CCUS over the next 6 years, for an additional 10 to 30 million metric tons of CO2 capture capacity. The 2018 legislation provides a tax credit of up to $50/Mt of permanently stored CO2 and $35/Mt for that used for EOR or other industrial uses, provided storage containment can be clearly demonstrated. It also removes any limitation on the amount of CO2 storage that can be claimed. It is considered a monumental achievement and is one of several recent policy developments and financial incentives providing encouraging signs for Japan, The Netherlands, Norway, the UK, Saudi Arabia, China, and the European Union.

However, many companies who wish to take advantage of the credit say inconsistencies and the absence of consistent guidance, which could help guide investment decisions, has added to the challenge of project development. In many cases, inability to reach final investment decision (FID) is believed to result from concerns of equity/debt holders over uncertainty about the consistency and tenure of the tax credits.

Unlocking CCUS Investment

The IEA’s recently published Five Keys to Unlock CCS Investment includes the following.

- Harvest “low-hanging fruit” to build CCS deployment and experience from the ground up.

- Tailor policies to local conditions to shepherd CCS through the early deployment phase and to address the unique integration challenges for these facilities. Many of the sectors where CCS will be required, including steel and cement, operate in competitive international markets where additional costs associated with CCS cannot be passed on to consumers.

- Target multiple pathways to reduce costs. Cost reduction through learning by doing at scale is proving, in practice, to have a large impact. External project financing has played a relatively minor role in CCS investments to date, but will need to expand to support future widespread deployment. Capital markets have an increasing appetite for low-carbon assets, but CCS remains a relatively unfamiliar technology for most financiers. The cost of financing can be reduced not only with increased project experience and reduced technology risk, but also through progressive financing arrangements and the involvement of international financing institutions or export credit agencies, which can offer near-zero interest rates or loan guarantees.

- Build CO2 networks and accelerate CO2 storage assessments in key regions.

- Strengthen partnerships and cooperation between industry and governments. Policies are required to alter behavior, said the GCCSI in its 2018 Global Status of CCS Report. Policy—which encompasses mandates, tax credits, direct subsidies, loan guarantees, and more—can enable governments to achieve their objectives while supporting the business case for investment in CCUS and winning the confidence of investors, which is critical for long-term capital investments. Once these investments are made, investment and cost reduction will accelerate, along with the pace of scale-up that is necessary to meet climate, clean air, and business objectives.

Game ChangersThe following technologies and projects are considered game changers with promise to accelerate uptake of CCUS. Allam cycle technology is a process for converting fossil fuels into mechanical power while capturing the generated CO2 and water. It is the enabler of NET Power’s 50‑MW first-of-its-kind, emission-free natural gas-fired power plant in Texas. The Allam cycle uses a single turbine, driven by a working fluid consisting of only water and CO2, which is achieved by using pure oxygen instead of air to burn the fuel. The exhaust gas is cooled in a heat exchanger, and the steam is condensed and separated from the flow, becoming a potential source of fresh water. The carbon dioxide is compressed mechanically, and a small amount, matching the amount continuously added through combustion, is captured at high pressure, ready for pipeline transmission. The rest of the CO2 is reheated in the heat exchanger and recycled into the combustion unit, where it continues to form the vast majority of the working fluid. The NET Power demonstration project began operations in 2018, and it is hoped that it could eventually make zero-emissions coal- and natural gas-fired power generation competitive with existing power generation technologies. Direct air capture (DAC) uses capture technologies that bind or “stick” to CO2 to capture it directly from the air rather than at industrial sources. Concentration of CO2 is lower with DAC than at industrial sources, which presents engineering challenges, and the technology is still quite immature. However, combining DAC with carbon storage could act as a carbon dioxide removal technology and as such would constitute a form of climate engineering if deployed at large scale. DAC technology operates successfully at Zurich-based Climeworks, Carbon Engineering in Canada, and Global Thermostat in the US. Fuel cell energy technology, developed by the Fuel Cell Energy Company, aims to capture CO2 using a system of molten carbonate fuel cells, which the company believes could capture CO2 more efficiently than other capture technologies. The system capturing CO2 from the flue gas stream of a host plant would also generate electricity, thereby circumventing the parasitic load cost associated with traditional carbon capture on power plants. The Drax bioenergy CCUS pilot project in the United Kingdom is a world-first demonstration that captures CO2 from a power plant fueled by 100% biomass feedstock. The pilot began operations in early 2019, and if successful it could become the world’s first negative-emissions power station. Cemvita Factory’s CO2 utilization platform uses CO2 as the carbon feedstock to mimic the complete photosynthesis process by simultaneous uptake of solar energy, water, and processing of carbon dioxide to produce nutrients, pharmaceuticals, intermediate chemicals, and polymers. |

Carrots and Sticks

While tax credits, grant funding, external financing, and other “carrots” to unlock CCUS investment are the subject of widespread discussion, there is also a lot of talk about “sticks” ranging from carbon taxes on producers to consumption taxes on households. The 13 member companies of the CEO-led Oil and Gas Climate Initiative (OGCI) have announced that they are ramping up the speed and scale of their actions in support of the Paris Agreement, and all member companies have pledged to support policies that attribute an explicit or implicit value to carbon.

The bottom line, say many, is that addressing emissions—and by association, CCUS—is a universal challenge that will require collaboration, cooperation, and compromise on the part of all stakeholders.

An excellent example of success is the Shell-operated Quest carbon capture and storage facility near Edmonton, Alberta. In its first four years of operation, Quest has captured and safely stored 4 million Mt of CO2—equivalent to the annual emissions of about one million cars—and has achieved this milestone ahead of schedule and at a lower cost than expected. Shell says Quest has stored more carbon dioxide than any other similar project in the world and is doing it at a higher annual rate. The facility captures and stores underground about one-third of the CO2 emissions from the Shell-operated Scotford Upgrader, which turns oil sands bitumen into synthetic crude that can be refined into fuel and other products. The project opened in 2015 and cost about $1.35 billion, backed with $745 million from the Alberta government and $120 million from Ottawa. Shell also began receiving two-for-one carbon credits for a ten-year period in 2017. Additionally, Shell says support from the local community was essential to building Quest. To that end, the company initiated public consultation in 2008, two years before submitting a regulatory application.

An article by Bryant published in the September 2007 issue of JPT was titled, “Geologic CO2 Storage—Can the Oil and Gas Industry Help Save the Planet?” When interviewed recently, Bryant said he would use the same title today and focus on what he calls the “exciting new technologies” that will directly offset carbon content rather than avoiding emissions.

“The window of getting things done gets shorter every year, and the perfect is the enemy of the good,” said Bryant. “We don’t have the luxury of waiting any longer for the solution. We need to build things we know will work now.”