Energy is vital to human flourishing. Since the dawn of time, humans have sought to find more efficient ways to power and propel their lives forward. With each generation, we’ve made progress in unlocking energy density—moving from burning wood for warmth inside caves thousands of years ago through our current age, where a revolution in modern energy is transpiring.

However, recent global events have certainly tested the upstream oil and gas sector’s “can-do” attitude and spirit of innovation.

In the 3 years since West Texas Intermediate Crude (WTI) futures dipped below zero—dropping more than 300%—to settle at negative $37.63/bbl, there has been a global COVID-19 pandemic and recovery, supply chain and logistical challenges, and a war.

The oil and gas industry is more adept at riding the market volatility wave than in the past. WTI futures climbed out of the negative, reaching as high as $123.70/bbl on 8 March 2022, as the pandemic began to ease, and the lockdown ended in many regions worldwide.

Geopolitical tension with Russia and its full‑scale invasion of Ukraine in the first half of 2022 contributed to the crude oil price increases. Also contributing to higher pricing in the first half were concerns over supply levels. The Russian invasion of Ukraine came during eight consecutive quarters of crude oil level decreases, according to the US Energy Information Administration (EIA).

In the year since, the price has dropped but not nearly as profoundly, with recent prices ping-ponging in the mid-$60 to mid-$80/bbl range. The EIA cited as reasons for the lower price concerns over a possible economic recession and China’s severe COVID-19 containment measures as keeping global demand lower.

The Russian invasion of Ukraine turned global markets upside down. The International Energy Agency (IEA) cited it as the trigger of a worldwide energy crisis that “has the potential to hasten the transition to a more sustainable and secure energy system,” in its World Energy Outlook 2022.

“Energy markets and policies have changed as a result of Russia’s invasion of Ukraine, not just for the time being, but for decades to come,” said IEA Executive Director Fatih Birol at the time of the outlook’s release. “Even with today’s policy settings, the energy world is shifting dramatically before our eyes."

Transition and Trilemma

The energy transition changes how the world views and uses oil and gas. While it is not the first energy transition the world has faced, it is proving to be the most significant and complicated.

“It is needed if we are to prevent the 1.5°C increase in temperature,” Kjetil Hove, the executive vice president of development and production in Norway for Equinor, said during his keynote address at the SPE/IADC International Drilling Conference and Exhibition held in Stavanger on 7 March.

“The future carbon intensity of the energy mix needs to be reduced significantly. Last year’s energy crisis and the war in the middle of Europe showed that the energy transition needs to be done wisely and that it addresses the energy trilemma,” he said.

This energy trilemma is a concept that speaks to the intricate nature of energy production. To be successful, energy providers must find ways to balance energy security, affordability, and environmental protection.

For oil and gas companies, this means finding a way to meet their sustainability goals while still providing reliable energy sources to consumers. This can be difficult as often these goals directly contradict each other. It’s a balance of priorities. Affordable energy must be low-cost and accessible to all. This, however, is often at odds with sustainability as the cheapest energy source may be the most polluting.

Dollars and Sense

Hove noted that since adopting the Paris Climate Accords in 2015, the focus has changed from mainly sustainable energy to now with more emphasis on energy security and affordability.

“The world needs a sustainable energy policy. We need large growth in renewable energy. We need large growth in low-carbon solutions,” he said. “However, we will also need oil and gas for decades to come.”

Investments in clean energy have increased and now represent a 1.5:1 ratio with fossil fuels. Still, these investments need to be scaled up dramatically, to a ratio of 9:1 by 2030 to be consistent with the net zero path, according to the IEA’s World Energy Investment 2022.

These investments are necessary to ensure the long-term viability of the oil and gas industry. However, so too is the continued investment in oil and gas production.

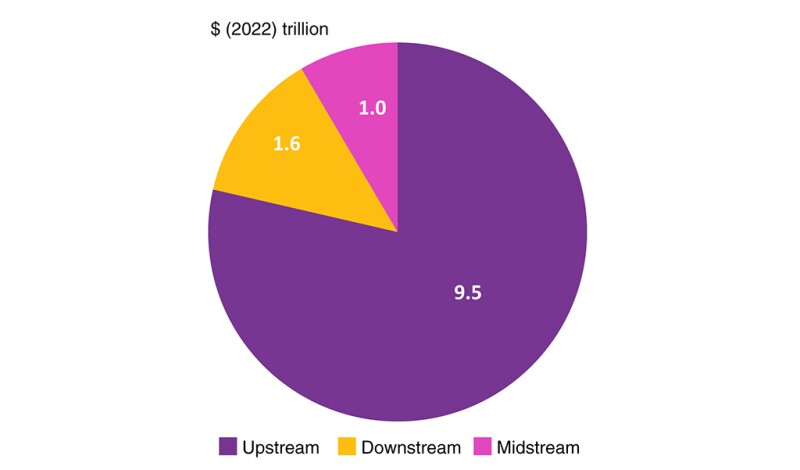

In its 2022 World Oil Outlook 2045 (WOO), OPEC said trillions of dollars’ worth of investments in the oil industry would be needed over the next 2 decades to meet the rising demand for hydrocarbons.

“To place expected future energy demand in some context, the WOO sees the need to annually add on average 2.7 million BOE/D in the period to 2045. This requires huge investments. Moreover, for the oil industry alone, we also need to add 5 million BOPD every year to just maintain current production at around 100 million BPD, given an average annual industry decline rate of around 5%,” it said in the report.

“The overall investment number for the oil sector is $12.1 trillion out to 2045. However, chronic underinvestment into the global oil industry in recent years, due to industry downturns, the COVID-19 pandemic, and policies centered on ending financing in fossil fuel projects, is a major cause of concern (Figs. 1 and 2).

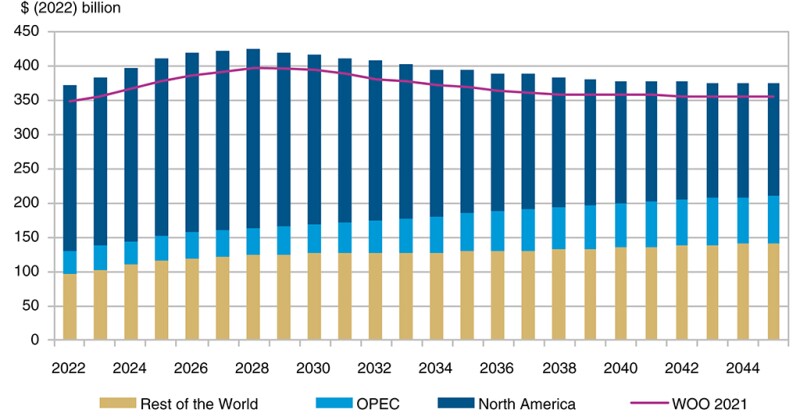

The International Energy Forum (IEF) and S&P Global Commodity Insights found that a cumulative $4.9-trillion investment in global upstream oil and gas is needed by 2030 to meet market needs and prevent a supply shortfall, even if demand growth slows toward a plateau, the groups reported.

The IEF said that the 2022 upstream capex increased by 39% to $499 billion, the highest level since 2014 and the most significant year-on-year gain in history.

“In the last year, energy security has trumped sustainability,” said Tom Ellacott, senior vice president of corporate research for Wood Mackenzie.

“Companies, too, have benefited from recent commodity prices and margins to deliver record cash flow. That is not to say that decarbonization goals cannot be met and priorities cannot change,” he said.

Ellacott added that to spur activity, there needs to be a “recalibration of current risks and rewards for investment in low-carbon technologies, as well as new incentives from government stakeholders and financial institutions. There’s no one answer, but smart oil and gas and natural resources companies will realize that protecting the status quo would be a mistake and start to manage their portfolios to reflect a balanced approach of managing legacy output and carbon management.”

According to “Fuelling Change” a new Horizons report from Wood Mackenzie, companies can address this complex dynamic in multiple ways, with the first one calling for “nurturing legacy cash cows while simultaneously shifting to a transition-growth mindset.

“Investors expect companies to balance the need for returns in the short term by tending to their legacy portfolio while delivering low-carbon transformation plans. Visibility of low-carbon profit centers starting to support—and supplant—the legacy cash cows could be a revaluation trigger that shifts the market to a transition growth mindset,” said the report’s authors. “Companies can scale back share buybacks to fund the shift. The mining majors and international oil companies allocated $157 billion, or 30% of their operating cash flow, to buybacks in 2022. Companies could still grow base dividends and lift reinvestment rates to over 60%.”

The good news regarding oil and gas investment is that it is set to continue in the year ahead. Spending by oil and gas upstream companies will rise above pre-COVID-19 levels in 2023. Still, it will remain about 40% below the 2013 peak of $608 billion, according to a Wall Street Journal report on a survey by the investment banking company Raymond James.

In its annual survey of companies representing about 70% of global output, Raymond James analysts found that these companies would spend $376 billion on oil and gas exploration and extraction in 2023.

According to the report, this is about 11% more than in 2022 and is the third straight increase in spending since it dropped in 2020 when the global economy was locked down to slow the spread of COVID-19 and energy prices crashed.

New Wells and Intervention

Hove noted in his remarks that Equinor’s ambition on the Norwegian Continental Shelf (NCS) is about “going from a pure oil and gas play to a broad energy province. By doing this, we will reach net zero.”

He added that the company plans to drill 20–30 exploration wells annually on the NCS and that “towards 2040, it is going to drill almost 3,000 new wells on the NCS.”

He said this activity level would maintain the value created on the NCS.

“However, we need to do it differently. In the future, what we are exploring and producing is different than what it was in the past,” he said. “Significant cost reduction is needed because the complexity of the reservoirs is increasing, and the size of the targets are decreasing.” He called on the industry to continue developing and innovating its technology.

“If we’re going to be successful in achieving the ambitions on the activity levels in decades to come, we need to continue the technology development that we have had within the industry for many decades to come,” he said.

Global oil and gas projects getting the green light and achieving a final investment decision (FID) is becoming more challenging than it used to be, according to a 12 April report by Wood Mackenzie.

“Despite a continued uptick in activity since the pandemic nadir of 2020, fewer major projects were sanctioned in 2022 than was expected at the start of the year,” the report said. “In 2023, we believe more than 30 of the 40+ viable major projects will likely reach FID. Several could be delayed and re-evaluated due to ongoing cost inflation; most operators will remain disciplined. A handful of lower-return projects will proceed because of their strategic importance.”

In its Class of 2023: Benchmarking This Year’s Upstream FIDs report, Wood Mackenzie forecasts that up to $185 billion of investment could develop 27 billion BOE of reserves. National oil companies will “dominate the year as they take advantage of huge, discovered resources and boast the lowest unit costs. The average unit development cost of $7.00/BOE in 2023 is down slightly from 2022.”

A key piece for any FID decision is carbon mitigation, with Wood Mackenzie finding that the “class of 2023 emissions intensity of 19 kgCO2 BOE is only just below the global onstream average of 22 kgCO2 BOE, but like that of 2022. Advantaged deepwater oil and shelf projects outperform; LNG, sour gas, and some onshore projects require mitigation but have broader Scope 3 advantages,” the report said.

To maintain the importance of continued exploration and discovery of new resources, equal importance should be given to producing wells. This point was brought up during the Operator’s Roundtable at the SPE/ICoTA Well Intervention Conference and Exhibition held in The Woodlands, Texas.

“There’s no doubt that intervention work is the cheapest barrels you can get out of the ground,” said Tony Ryan, manager of well intervention and integrity—USA for ConocoPhillips. “The well is already drilled. If you give it a bit of TLC and nurturing to get it back online, that’s the easiest a well can get.”

Not only does intervention provide the cheapest barrels, but it also helps lower emissions.

“Intervention gives the lowest carbon footprint to get a single barrel out of the ground because it has an opportunity to increase the recovery factor of every field,” said Mohd Abshar Mohd Nor, general manager for well intervention, Petronas.

Abshar explained that by increasing the recovery factor of aging fields, “we can keep using the same facilities without needing to decommission the field. We reduce carbon by squeezing more barrels out of the same facilities.

“It is about increasing how much you can extract from the fields and facilities that we already have rather than investing in new fields or drilling new wells,” he said.

The industry must continue to develop new technologies and innovations and maintain current technology to reach the ambitious activity goals of the future.

With carbon mitigation a critical component for any greenfield FID decision, innovation will be integral for success in the future. By continuing to invest in intervention activities, oil and gas operators can simultaneously reduce their emissions and increase their recovery factors. The challenge ahead is how to achieve this while maintaining efficiency and cost effectiveness.

In conclusion, oil and gas companies must continue developing new technologies, investing in intervention activities, innovating production methods, and applying carbon mitigation techniques if they will reach their ambitious activity goals while balancing the needs of ensuring a secure, affordable, and sustainable energy supply.