Editor’s Note: This is the second of a three-part series focusing on the contraction of the North American shale sector. Read Part I here.

If you created an endangered shale operator checklist, Templar Energy would check most of the boxes.

It was one of many companies started early in the decade by private-equity investors with a goal of profiting from shale acreage development

It was born in 2012 when $100/bbl oil looked like a given. The founding firm First Reserve’s announcement said it brought in an experienced leadership team led by a chief executive officer who had delivered on that plan before, David Le Norman.

The plan for companies like Templar was to lease promising acreage, drill some good wells, and sell to an operator for a large profit in a few years.

“Companies piled on debt, bought acreage, and developed it for sale,” said Buddy Clark, who co-chairs Haynes and Boone's energy practice group and primarily represents oil borrowers.

That plan hit a wall in late 2014 when the era of $100/bbl oil abruptly ended and the goal shifted to finding a way to make money at $50/bbl. The income from the wells Templar had mass-produced back when it had as many as 13 rigs working could not support the $1.7-billion debt it had accumulated.

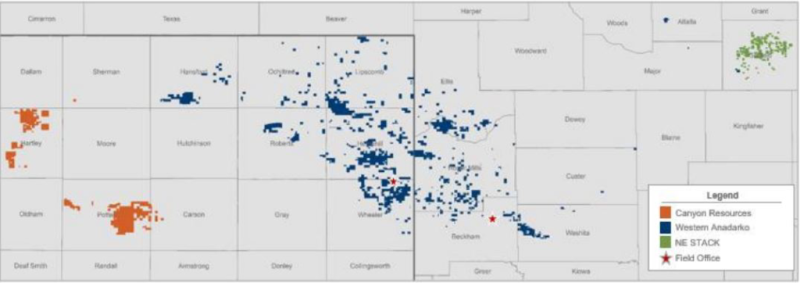

Templar Energy held 273,400 acres in the Western Anadarko, Canyon Resources, and Northeast STACK plays.Source: Templar Energy

Back then the shale creditors were generally willing to help lighten that load. Templar’s summary recently filed with its Chapter 11 bankruptcy protection case said investors agreed to reduce its debt by $1.4 billion in exchange for 45% of the Templar stock and $133 million of the $365 million in cash raised by selling shares to recapitalize the company. At the time, the company could borrow up to $600 million from the bank.

The downside was Templar began its next era with less capital, as did many companies that restructured their loans back then.

“In 2016 and 2017 there were a lot of restructurings,” said Charlie Beckham, a Haynes and Boone bankruptcy partner. He said, “There were doubts about whether they were fixing the problem” because many of the restructurings resulted in a lot of debt left on the books of E&P companies. They assumed that by 2019 and 2020 commodity prices would have bounced up and strengthened those balance sheets.

Instead, by 2019 prices were still down around $50/bbl and the expected oil production per acre had sunk because plans to maximize production with tightly spaced arrays of wells and massive fractures fell far short of expectations.

Templar’s oil production fell to half the level at its peak in 2016, based on production reports from the data service Shale Profile.

After bankers completed their semiannual evaluation of the reserves in April 2019, they informed Templar that the reserves securing its $437-million debt were worth $415 million—meaning it would all come due later in the year, according to the summary.

The summary was signed by Brian Simmons, the chief executive officer who replaced Le Norman that April. It described how he worked to improve Templar’s financial condition by selling 12 saltwater disposal wells to raise cash. He cut costs by replacing gas lift systems with lower-cost rod pumps, saving $750,000 a month.

Despite these initiatives, revenue and cash flows continued to decline and “it became clear that there was no scenario where recapitalizing the debtors’ business would be feasible absent a restructuring” its debts, the company summary said.

Creditors were asked for another round of concessions, but the talks ended with an agreement that “a sale of all or substantially all of their assets would be the most value-maximizing alternative.”

Templar is not unique in that. “We are seeing some of that also,” said Clark. When the value of the reserves drops below the value of the of loan, “bankers are less interested in being long-term holders than investors” who likely bought the note and bonds at a discount. The result is a bankruptcy where the plan is to “just sell what you have got,” he said.

By late last year, Templar had contacted 150 potential buyers and 41 had signed nondisclosure agreements allowing them to evaluate the assets in its online “data room.” Bids for all or parts of the company were due in March.