The World Offshore Operations & Maintenance Market Forecast 2012–2016 forecasts more than USD 335 billion expenditure over the next 5 years on offshore operations and maintenance (O&M). Douglas-Westwood’s report forecasts growth of 8% in expenditure annually from 2012 to 2016, with O&M markets considerably less vulnerable to downturn than their capital‑led counterparts.

Industry Drivers

Offshore O&M activity is driven by a variety of supply-side and demand-side factors, such as:

- Growth in global energy demand that, in the medium term, means demand for hydrocarbons. The long-term trend toward increasing energy consumption is clear.

- As onshore reservoirs continue to mature and new prospects become few and far between, a greater proportion of oil and gas production will be met by the offshore sector.

Cost inflation and oil price fluctuations do not generally have the same level of impact on O&M expenditure compared with capital expenditure-related activities such as drilling and field development. This is mainly due to O&M expenditure being vital to ensuring the maintenance of ongoing production levels, the principal revenue stream for offshore operators. Douglas-Westwood expects that the majority of the markets in the report are considerably more robust than those relating to the initial development of oil and gas fields with any significant upturns or downturns in global expenditure being driven principally by industry cost inflation (or deflation).

A number of the services, such as well stimulation, wireline operations, subsea well intervention, and platform drilling are highly price sensitive and their economic viability is dependent upon a number of criteria including oil price, vessel/unit/rig rates, and potential upside in oil or gas flow rates.

Market Forecast

Offshore O&M covers the following sectors:

- Operations: Services required for ongoing production, including the supply of labor and raw materials

- Production services: Power generation, produced water management, wireline services, and stimulation services

- Support services: Hotel services, deck crew, and miscellanous personnel

- Platform drilling: Rig and crew, well construction, integrity and consumables

- Logistics: Crew boat, platform supply vessels, and helicopters

- Maintenance-related

- Asset services: Fabric maintenance and floating platform lease market

- Subsea inspection, repair, and maintenance: Field-related, subsea well intervention, and subsea asset integrity

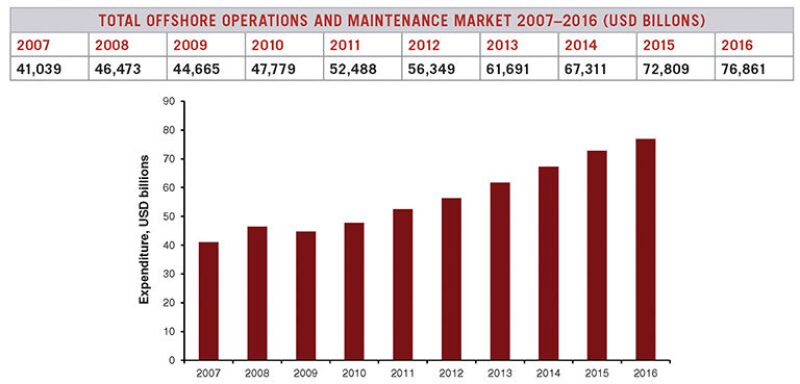

In 2011, the demand for offshore O&M services totaled more than USD 52 billion, having grown at a compound rate of more than 6% over the past 5 years. Over the next 5 years, Douglas-Westwood expects a greater level of growth as the market recovers from the effects of the global downturn of 2008 to 2009. It will be driven by a combination of high oil prices, buoyant offshore development activity, and rampant price inflation for equipment and services.

O&M markets are considerably less vulnerable to downturn than their capital-led counterparts. While global offshore drilling activity dropped by an estimated 14% between 2008 and 2009, total offshore production (the principal driver for all operational activity) grew by 1%. The global offshore O&M market fell, but only slightly, despite widespread price deflation for equipment and services.

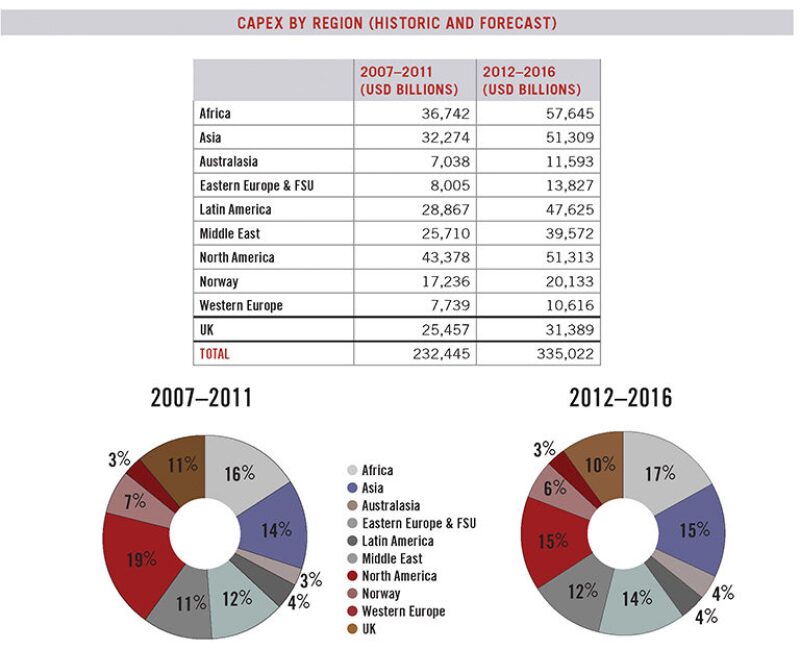

Historical dominance of mature western basins is to be challenged. Between 2007 and 2011, 40% of global O&M demand was accounted for by western Europe and North America. Although market growth is expected in all regions (despite the United Kingdom and the rest of the western Europe regions facing terminal production decline), Douglas-Westwood expects the western Europe and North America share of global demand over the forecast period to drop by a few percent. This shift will be driven by a combination of increasing offshore production in regions such as the Middle East and the movement toward deep water in less mature regions such as Africa and Latin America.

Conclusions

- Production services dominate O&M market expenditure. Over the period from 2007 to 2011, production-related services accounted for 44% of global O&M demand. These services are directly associated with production levels from offshore facilities and are intensified as an oil or gas reservoir matures and requires additional effort to sustain production. The inevitable maturing of offshore fields will drive compound growth of more than 7% in the production services sector as operators struggle to come to terms with decreasing downhole pressures and increasing water cuts.

- The asset services market is set to outgrow all other market sectors. In particular, the trend toward leasing of floating production systems (FPS) has led to substantial growth in this sector. Between 2012 and 2016, 136 new FPS units are expected to be installed, of which more than half are likely to be leased. This will drive significant growth in the asset services market over the next 5 years.