The war in Ukraine is likely to accelerate the global energy transition as oil and gas importers seek greater energy security by shifting to renewable energy sources that can be produced domestically, BP’s Chief Economist Spencer Dale argued while unveiling BP’s benchmark Energy Outlook 2023 in a global webcast this week.

Ukraine was one of three areas Dale highlighted at the 30 January launch along with the impact of the Inflation Reduction Act (IRA) which supports development of low-carbon energy and technologies in the US, plus four global trends that are driving the future of the energy industry.

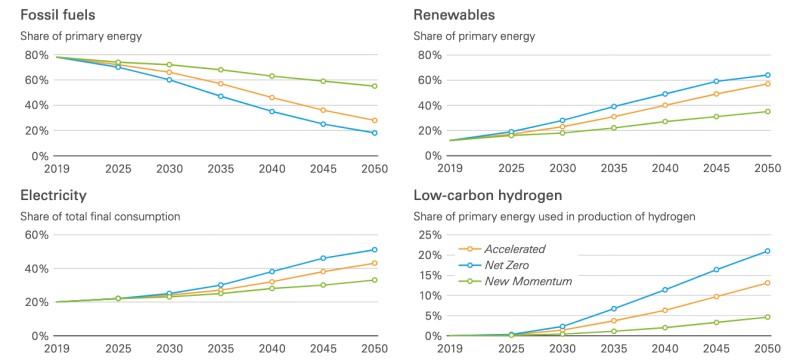

- The declining role of hydrocarbons

- A rapid growth in renewable energy

- Increased use of electricity as an energy source, particularly in transportation

- Growth in the use of low-carbon hydrogen

Four Global Energy Trends That Will Shape the Future

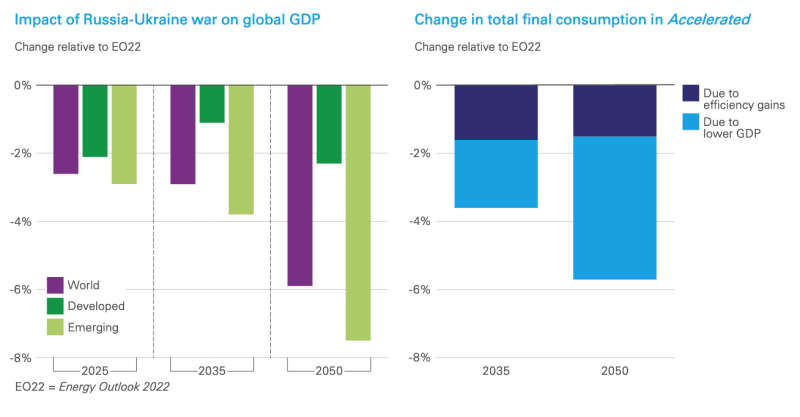

But the war in Ukraine, Dale said, is “for me the most significant” … because “the disruption to Russian energy supply and resulting energy shortages … is pointing out the need for the energy transition to address … the trilemma of energy security, affordability, and sustainability.”

Thus, he said, “This year’s Outlook has a special focus on the implications of the war,” pointing out that among those implications is a 3% slowdown in global economic activity by 2035 as compared to BP’s 2022 forecast: a slowdown driven by rising energy and food prices as well as supply chain disruptions. The impact of the conflict demonstrates the need for an orderly transition away from hydrocarbons, Dale said.

Forecast Effects of the War in Ukraine on Energy Consumption

Dale likened the current situation to that of the 1973 OPEC oil embargo which saw a massive buildout of nuclear power in France and the US decision to create a strategic oil reserve to cite two examples. In the near term, the war in Ukraine is even now resulting in national policy changes; long term, fallout from the conflict will slow the pace of globalization and the integration of economies that “will lead to slower growth over the next 30 years,” he added.

As for Russian energy supplies … “for this year we assume a decrease in Russian exports. Near-term this is on the demand side; farther out it will be felt on the supply side because of the financial effects” of investment lost to sanctions, BP’s chief economist said.

Downward Revision of Russian Oil and Gas Production

One big unknown, however, is the future role of natural gas. “The broad direction of travel is clear: oil and coal are down. The prospect for natural gas is much less clear,” Dale said, considering the role that natural gas plays in the production of hydrogen as an aviation and bunker fuel, and rising demand for liquefied natural gas (LNG).

BP’s report estimates the evolution of energy supply and demand based on a consideration of three scenarios—New Momentum, based on a continuation of the existing trend— plus Accelerated and Net Zero, where assessments are based on graded scenarios of faster transitions away from fossil fuels. Thus, many details in the forecasts are expressed as a range of data points.

Near-Term Bonanza for US LNG

LNG exports from the US and Qatar are forecast to meet growth in global LNG demand through 2030 with growth in US exports accounting for between half to two-thirds of the supply increase depending on which scenario is considered. By 2030, the US and the Middle East together account for around half of global LNG supplies, as compared to their filling only a third of demand in 2019.

However, US LNG exports are forecast to fall by more than half between 2030 and 2050 because of increased competition and higher transport costs for US supplies bound for Asia, a reality that hands the advantage to LNG volumes from the Middle East and Africa.

Australian LNG exports decline after 2030 because of cost and constraints on upstream natural gas production in Australia. As for Russia, exports could double between 2030 and 2050, assuming sanctions disappear, but by then LNG demand could be in decline and market opportunities lost, according to BP’s Outlook.

US and Middle East Dominate LNG Exports Through 2050