Prior to 2012, water management for unconventional oil and gas plays was in its infancy and was trying to keep up with operations. Questions about the scale of the unconventionals, water-sourcing limitations, economics of water reuse, infrastructure needs, and sustainability were already being considered. Industry volatility, seismicity, and regulatory challenges were major factors continuously during this evolution. Today, many of the initial challenges have been resolved but new challenges persist. Regional water management variations and challenges are apparent. What does the future hold for water in the US onshore unconventional plays?

Water Management 10 Years Ago

Water management for the US onshore unconventionals has come a long way in 10 years. In the 2011–2012 timeframe, it was still not clear which shale plays would be most viable. Some plays like the Barnett and Haynesville have come, gone, and come back again.

In the Permian 10 years ago, operators were asking where they would get the water to complete thousands of wells. Produced water reuse was mostly being evaluated in pilot tests by producers such as Apache, Devon, and Pioneer, but was not considered viable due to the high cost of treatment and transportation by truck. Much of Texas and the West was experiencing a significant drought that also raised concerns about water sourcing for hydraulic fracturing.

Despite these challenges, sustainability was considered a factor in these new development areas, but usually was not sufficient to override cost differences.

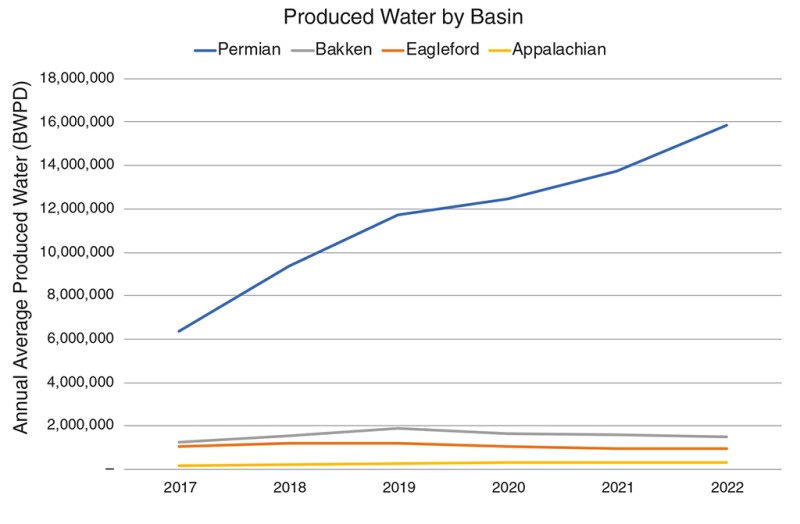

Ten years ago, it was apparent that each basin had unique water management considerations. Some basins such as the Bakken and Marcellus had significant surface water sources available, whereas Texas, Oklahoma, and New Mexico were regularly quite dry. Most areas had good formations available for disposal, with Pennsylvania and West Virginia being the exceptions. A third area of difference was how much produced water flowed from the new wells. The wells in the Permian stood out as having the highest water/oil ratio seen in US onshore production. All of these differences impacted how each region was best able to manage its water challenges.

In 2012, the water management strategy to build out water pipeline networks to move large volumes of water was not yet seriously considered by most operators. Earthquakes were not a significant factor in any of the US basins.

However, some of the water management issues were changing. For example, the historically independent nature of producing companies began to change as water challenges became viewed as shared problems. Regional water groups were established as companies began to share ideas pertaining to water management.

The Energy Water Initiative (EWI) was formed as a group of oil and gas companies trying to improve water practices. Their 2015 report on water management case studies broke new ground for industry collaboration. The EWI report documented seven trends including the ability to use non-freshwater sources and technology innovations making produced water reuse more feasible.

Water Management 5 Years Ago

Jumping ahead 5 years to around 2017, several macroeconomic events impacted water management for unconventionals. Perhaps most notable was the dramatic oil price collapse in late 2014 from roughly $100 to about $50/bbl. The increase in US onshore oil and gas production impacted global oil prices. The lower commodity pricing resulted in substantial pressure on costs, including water sourcing and disposal. At the same time, producers were increasing the length of horizontal wells and the volume of water required to complete the well.

The key concern shifted from where to source the completion water necessary, to where to dispose of all the produced water. Earthquakes became a significant challenge in some basins. Oklahoma measured minimal earthquakes prior to 2009 but had over 800 earthquakes greater than a 3.0 magnitude in 2016.

State regulators took a series of actions to limit disposal to reduce seismicity risks. By 2017, Oklahoma’s earthquake frequency was falling. The Oklahoma Produced Water Working Group published a report related to produced water and beneficial reuse in 2017. The group was one of the first to have significant involvement of regulators, industry, and environmental nongovernmental organizations (NGOs).

The key findings included:

- Produced water reuse in oil and gas operations was the most viable alternative to disposal.

- Beneficial reuse through desalination was technically viable but economically impractical.

- Produced water evaporation techniques should be further investigated and developed.

In the Permian Basin, the scale of the activity was driving producers and water midstream companies to build out large networks of water infrastructure to move water more effectively and at lower costs compared to trucking. Concurrently, high-volume slickwater completions became the standard. This completion design did not require water of as high quality as the gel fracs from prior years.

This combination of cost pressure, infrastructure, and water quality began a trend of increasing water reuse. Water reuse is produced water used in a completion of a subsequent well. Water reuse was estimated at around 10 to 15% 5 years ago in the Permian. In a limited number of cases, demonstrations proved that individual frac jobs were successful with up to 100% reuse water, with the percentage varying by local logistics or company, among other drivers.

By 2017, the number of Oklahoma earthquakes above a 3.0 magnitude had fallen 69% from their peak year. In the Permian, earthquakes above a 3.0 magnitude were still quite rare. More ground‑shaking changes were coming.

Centralized water networks, often managed by water midstream companies or producing company water teams, were growing and would be part of better water management practices. This extended into the core areas of most of the US onshore basins with substantial drilling activity.

Regulatory changes by the US Environmental Protection Agency and state regulators helped encourage produced water reuse in some cases. Produced water began to be considered an asset instead of always being a waste. Multiple states passed rules that allowed the produced water liability to pass along with the custody, thereby encouraging companies to share or exchange water.

Water Management Today

Today, water management in unconventionals continues to progress. Reuse for subsequent wells in the Permian is reported to average about 30% according to B3 Insight. Many larger companies report over 50% reuse in the Permian, including Apache, Chevron, Pioneer, and Coterra.

The continued growth of water networks in most basins has reduced water trucking and allowed more flexibility for reuse or disposal. Water midstream companies are now consistently treating and delivering produced water for reuse. These larger networks are efficiently moving water and avoiding the problems of isolated operations. For example, XRI, a large water midstream company with operations in the Permian, emphasizes recycling produced water and presently treats and reuses 1.1 million B/D. XRI Vice Chairman John Durand stated, “Our infrastructure allows flexible use of large-scale water volumes required with multiwell pad drilling and multi-frac drilling operations.”

Select Energy Services is an oilfield service company that operates in and around the midstream water sector. “With just shy of 3 million barrels of daily produced water treatment capacity in the Permian and DJ basins, along with hundreds of miles of pipeline infrastructure dedicated to produced and brackish water movement, Select is capable of offsetting large volumes of freshwater usage as well as eliminating millions of truckloads of water from the roadways” said Rick McCurdy, vice president of innovation and sustainability at Select.

Even with increased reuse in the Permian, disposal volumes have continued to climb. With the increased water injection, seismicity has become problematic.

During the first 9 months of 2022, the Permian Basin had 169 earthquakes above a 3.0 magnitude. Most of these tremblors occurred in Culberson, Reeves, and Loving counties. This compares to only three earthquakes in the Permian above 3.0 in the first 9 months of 2017.

The 2019 Groundwater Protection Council report on produced water evaluated the state of water management and potential for beneficial reuse outside of oilfield operations. Some of the key conclusions were:

- Operators and regulators alike are rethinking the economics and long-term sustainability of traditional produced water management practices.

- While most near-term alternatives focus on reuse of produced water to reduce freshwater consumption in unconventional oil and gas operations, interest is growing in the potential for reuse outside the oil and gas industry.

This continued the trend of having regulators and stakeholders work together. Today, New Mexico and Texas both have consortiums evaluating beneficial reuse. The hope is that new water can be created in semi-arid areas for use by the broader community and water injection in saltwater disposal wells could be reduced. Additionally, there is hope that beneficial minerals could be extracted from the process.

Aris Water, a water midstream company, recently announced a strategic agreement with Chevron and ConocoPhillips to develop cost-effective and scalable methods of treating produced water to create a new water source for potential use in beneficial reuse. Aris Water CEO Amanda Brock said, “This joint agreement focusing on water treatment has the potential to drastically improve access to water in our local community. As the forecast for water usage continues to increase and drought conditions expand, it is imperative that new water sources are identified and optimized. With our partners, we will be evaluating and optimizing multiple technologies to establish a process that will scale economically.”

Looking back at 10 years of water management changes, much progress has been made. A dramatic shift to moving water by pipe instead of by truck has occurred. Reuse of produced water in subsequent fracs has increased significantly in key basins like the Permian.

The biggest challenges today are to manage water costs, drought in some areas, and seismicity in the Permian. Industry is likely to continue to build out water pipeline networks that will allow additional reuse.

Opportunities are being evaluated to consider beneficial reuse and mineral extraction from produced water. Companies are sharing more information in sustainability reports and annual reports about water management to demonstrate how progress continues to be made. We also project that the continued consolidation of companies and water networks will positively impact water management efficiencies. We also believe that beneficial reuse outside of oil and gas operations can become viable and will grow.

The path toward better water management for unconventionals has not been easy or a straight path. However, the progress over 10 years has been remarkable and the future suggests more positive evolution. Costs, regulations, and disposal limitations are likely to be the drivers of the next wave of changes for water management.

Michael Dunkel is an energy and water management advisor for Tetra Tech. He has focused on water management for upstream and midstream for over 10 years and has been a member of SPE for 40 years. He can be reached at Michael.Dunkel@TetraTech.com.