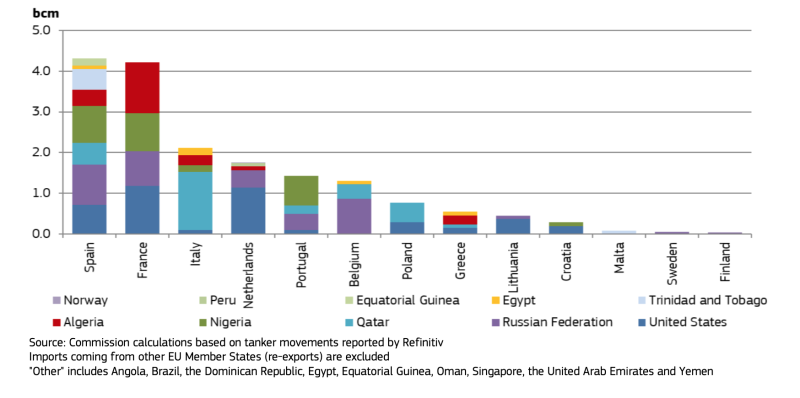

The United States remained Europe’s top supplier of liquefied natural gas (LNG) in the first 3 months of 2021 as it continued to gain market share at the expense of Russia and Qatar, Europe’s second- and third-largest sources of LNG, according to the EU Commission’s latest European Gas Market Report.

The US supplied 24% (4.2 Bcm) of the EU’s overall LNG imports (17 Bcm in Q1 2021); Russia placed second at 21% (3.7 Bcm); and Qatar was third at 18% (3.1 Bcm), the EU Commission reported in early July.

When compared to Q4 2020, the US picked up 2% market share from January to March this year, while Russia bested Qatar to become Europe’s second-largest LNG supplier. Nigeria placed fourth, followed by Algeria and Trinidad and Tobago.

A review of EU Commission reports dating back to 2019 reveals a steady quarter-to-quarter decline in Europe’s LNG purchases while it also documents the growing rivalry between the US and Russia, Qatar’s fall from dominance, and the emergence of the US as Europe’s top LNG supplier starting Q4 2019.

The EU is the world’s third-largest LNG market, though its imports amounted to only about half that of Japan (36 Bcm) and China (32 Bcm) in Q1 2021.

European gas consumption rose 7.6% to 132 Bcm in Q1 based on a year-on-year comparison. The commission noted that demand for gas as fuel to generate electricity rose 3.4%, also year-on-year (increasing by 4.9 TWh.)

In terms of gas deliveries overall, including pipeline gas, Russia remained the leading gas supplier to Europe (45% of all imports) with the Nord Stream 1 pipeline across the Baltic Sea as its most important supply route.

Nord Stream accounted for 41% of Russian pipeline imports (15 Bcm of gas transit) in Q1 2021. Transit across Belarus accounted for 29% with transit via Ukraine at 22% (8 Bcm). Turk Stream accounted for 8%. (Construction of Nord Stream 2 is scheduled for completion in August though commissioning of the twin lines to double capacity along the route remain in limbo while the US and Germany negotiate terms for lifting of US sanctions.)

After Russia, Norway was Europe’s second-largest gas supplier (23% of all imports) on the strength of its pipeline deliveries; Norway’s LNG sales were inconsequential (0.2% of EU purchases in Q1, 2021) but are likely to reboot in October when the Hammerfest LNG plant (damaged in a fire in September 2020) is again operational, the EU Commission noted.

LNG figured as Europe’s third-largest source of gas imports and is likely to play a larger role in the future as Europe’s largest domestic gas producer, the Netherlands, prepares to end production at its Groningen field in 2022.

The Netherlands produced 6.1 Bcm of gas in Q1 2021 followed by Romania, 2.4 Bcm; Poland, 1.4 Bcm, and Germany 1.2 Bcm, according to the report.

Anticipating the inevitable, operators of the Zebrugge LNG terminal have already announced they will begin to expand its regasification capacity gradually between now and 2026 to facilitate more LNG imports into Belgium.

Asian gas markets had drawn LNG cargos away from Europe by offering high premiums in January, thus causing spot gas prices to spike on Gasunie’s leading TTF (Title Transfer Facility) virtual trading platform and other European trading hubs, a phenomenon last seen in 2018, according to the EU Commission.

Because of rising spot prices, Europe more than doubled its pipeline imports from Algeria year-on-year in Q1 2021, because the purchases were based on far more competitive oil-indexed contracts, the report noted.