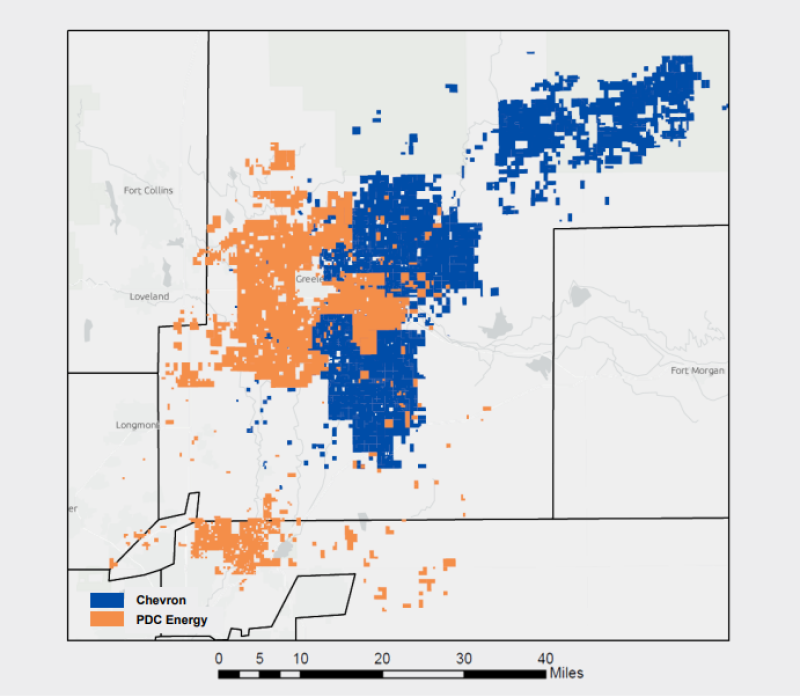

Chevron has entered into an agreement to acquire Denver-based PDC Energy in an all-stock transaction valued at $6.3 billion, or $72 per share. PDC’s assets include development opportunities adjacent to Chevron’s position in the Denver-Julesburg (DJ) Basin, as well as additional acreage to Chevron’s position in the Permian Basin. PDC’s 275,000 acres in the DJ Basin will add more than 1 billion BOE of proved reserves, while its 25,000 net acres in the Permian that are held by production will be integrated into Chevron’s existing development operations.

Based on Chevron’s closing price on 19 May, and under the terms of the agreement, PDC shareholders will receive 0.4638 shares of Chevron for each PDC share. The total enterprise value, including debt, of the transaction is $7.6 billion.

“PDC’s attractive and complementary assets strengthen Chevron’s position in key US production basins,” said Chevron Chairman and Chief Executive Mike Wirth. “This transaction is accretive to all important financial measures and enhances Chevron’s objective to safely deliver higher returns and lower carbon. We look forward to welcoming PDC’s team and shareholders to Chevron and continuing both companies’ focus on safe and reliable operations.”

The combined acreage holdings of Chevron and PDC Energy in the DJ Basin. SOURCE: Chevron.

Chevron expects to increase capex by around $1 billion per year, raising its guidance range to $14 to $16 billion through 2027, after realizing about $400 million in capex efficiencies post-closing. The transaction has been unanimously approved by the boards of directors of both companies and is expected to close by year-end 2023.

“Besides favorable ESG metrics and the immediate financial accretion that comes from buying from the smaller sized E&P peer group that has been discounted by the market, focusing on the DJ Basin likely allows Chevron to acquire undeveloped upside at more favorable pricing,” said Andrew Dittmar, director at energy market research specialists Enverus. “The company looks to have paid less than $5,000 per acre with more than 80% of the total deal value allocated to existing production. That compares to the Permian Basin where equity valuations for companies with equivalent inventory tend to be higher and M&A markets more competitive. Land containing equivalent quality inventory has priced at north of $20,000 per acre in recent M&A in both the Midland and Delaware basins. The Colorado assets do come with some increased regulatory risk, but the worst case for stopping permitting feared several years back has largely not come to pass.”

Over the past 5 years, PDC has been expanding its operations footprint in the DJ Basin through acquisitions of its own. Last year, the company purchased Great Western Petroleum in a stock and cash deal valued at $1.3 billion. The deal added acreage in the core western flank of the Wattenberg field in Weld and Adams counties in Colorado and immediately grew PDC’s production profile by 55,000 BOE/D.

In 2019, PDC scooped up SRC Energy in an all-stock deal valued at just over $1.7 billion, including debt. The deal added about 182,000 core acres in the DJ Basin, as well as adding to PDC’s position in the Permian.