The oil and gas industry is at a critical juncture in the evolving global energy landscape. As the world intensifies its focus on combating climate change and embracing renewable energy sources, traditional fossil fuel exploration faces unprecedented challenges. The energy transition is now a tangible reality, reshaping the foundations of the oil and gas sector.

However, just as there is no shortage of proclamations that the end draws near for King Fossil’s reign at the top of the energy resource pyramid, an equally high number sees the old king hanging around beyond 2050. This back-and-forth between renewable and fossil energy proponents gives all a good bone of contention to gnaw on.

In September, Fatih Birol, executive director of the International Energy Agency (IEA), wrote in the Financial Times that it is taboo to suggest that demand for fossil fuels could go into permanent decline. He announced that the relentless age of growth for fossil fuels is set to decline by 2030, according to new projections by the IEA set to be released this month in its World Energy Outlook.

OPEC criticized the announcement, describing the narrative as “extremely risky and impractical to dismiss fossil fuels or to suggest that they are at the beginning of their end.” The oil-producing nations group said the IEA’s thinking on fossil fuels is ideologically driven rather than fact-based, and predictions like these are “dangerous” because they are often accompanied by calls to stop investing in new oil and gas projects.

Upstream Investment: Too Little or Just Right?

The IEA and OPEC did find a small patch of common ground, agreeing that there would still be demand for oil and gas in 2050 and that continued investment in new oil and gas projects is needed.

The underinvestment in upstream asset development has been a concern for several years, with the COVID-19 pandemic only exacerbating the issue, and according to a recent report by Goldman Sachs, oil and gas activity declined at a compounded 7% from 2014 to 2021. The investment bank expects primary energy capital expenditure to grow 48% by 2027 to $1.9 trillion, up from $1.3 trillion in 2022.

“We believe the energy industry has been underinvesting since the peak of 2014, with investments in traditional energy (upstream oil and gas) falling 50% in 2020 from the peak and driving an 18% reduction in global primary energy investments, from $1.3 trillion in 2014 to $1.0 trillion in 2020,” the bank said.

“A number of oil and gas investment decisions had been delayed since 2014, translating into 10 million B/D of lost oil production by 2024–2025—equivalent to Saudi Arabia’s annual production—and 3 million BOED of lost LNG production—more than Qatar, on our estimates,” according to Goldman Sachs.

Despite these concerns, according to a recent Horizons report published by Wood Mackenzie, oil and gas demand can be met in the 2030s without a substantial increase to current annual investment levels of $500 billion.

Current upstream spending is “barely half of the $914 billion 2014 peak (in 2023 terms),” the energy consultancy wrote. This apparent shortfall, it said, fed a widespread belief that the industry is underinvesting and that a supply crunch is inevitable, be it sooner or later.

“We calculate that investment around today’s levels can deliver the supply needed to meet demand through to its peak and beyond,” said Fraser McKay, the report’s lead author and head of Upstream Analysis for the Edinburgh-based energy consultancy. “There are three main reasons: the development of giant low‑cost oil resources, relentless capital discipline, and a transformational improvement in investment efficiency.”

Wood Mackenzie predicts oil demand will eclipse pre-pandemic highs in 2023. From 2024, oil demand growth will slow, reaching a peak of 108 million B/D in the early 2030s.

“Conventional greenfield unit development costs have been slashed by 60% in 2023 terms, from $16.1/BOE in 2014 to $6.5/BOE in 2023, briefly dipping to a low of just $4.7/BOE in 2020,” said McKay, adding that “US tight-oil wells generate nearly three times more production for the same unit of capital than in 2014. New technology, capital efficiency, and modularization have been leveraged to powerful effect.”

For the rest of this decade, most of the industry’s oil and gas investment will target advantaged resources: those with the lowest cost, lowest emissions, and least risk, according to McKay.

“Non-OPEC supply growth is still dominated by the US Lower 48, which is now maturing and edging towards a plateau, augmented by deepwater Latin America (Brazil, Guyana, Suriname) and emerging giant plays such as Namibia,” said McKay. “OPEC aims to add around 3 million B/D of oil, primarily from Middle East expansion projects in Saudi Arabia, the United Arab Emirates, and Iraq.”

He added that the growth potential of these prime, existing, and advantaged opportunities will be exhausted beyond this decade and that new supply will become more expensive to develop.

“To meet demand, the industry will depend increasingly on late-life reserves growth from legacy supply sources, higher-cost greenfield developments, and as yet undiscovered volumes,” he said.

Exploration Keeps the Project Conveyor Belt Rolling

It has been a slower ride these past few years for marine seismic companies as the challenging oil and gas market has kept explorers waiting for better conditions to emerge in the sector.

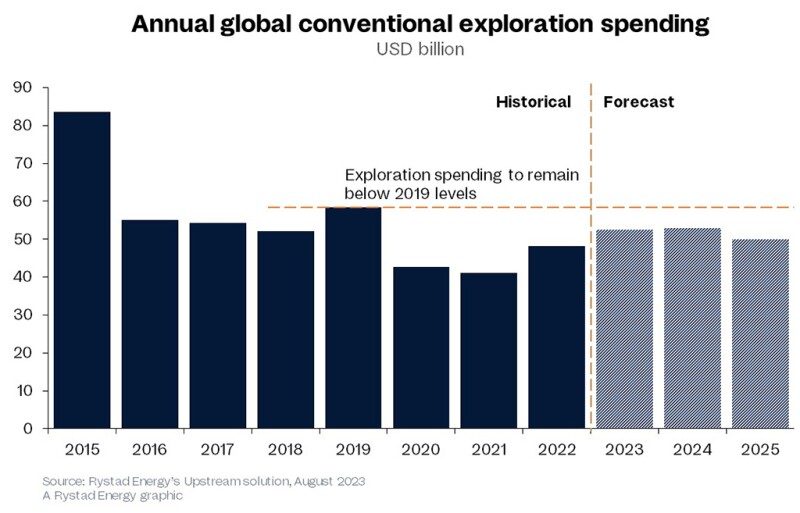

The wait appears to be ending as spending on conventional oil and gas exploration is rebounding, according to Rystad Energy. The Oslo-based energy consultancy expects spending to top $50 billion in 2023, the highest since 2019.

Wood Mackenzie also sees exploration spending to continue recovering from historic lows to an average of $22 billion per year over the next 5 years. It cited the need for energy security and the emergence of new frontiers as incentivizing oil and gas companies, led by the national oil companies and majors, to increase exploration spending.

“Explorers will become bolder in the coming years. While this rebound might surprise some, it must be seen in context. Exploration boomed during 2006–2014, and spending peaked at $79 billion (in 2023 terms). But in the prior 6 years, the average was $27 billion per year in 2023 terms,” said Julie Wilson, director of global exploration research at Wood Mackenzie.

“While spending will increase, it won’t return to anywhere close to past highs, and there will likely be a ceiling on the increase. There is a lack of high-quality prospects that would satisfy today’s economic and ESG metrics, and a continued focus on capital discipline will keep a lid on overspending,” she said.

David Hajovsky, executive vice president of the Western Hemisphere with TGS, sees the current exploration environment as one of recovery.

“If you go back a few years, the outlook was significantly more negative. We’re in a space now where you see the investment community and some companies realizing they need to build inventory and find new fields because the depletion rate on our current fields—if you’re going at an 8 or 10% year-on-year—will require a big backfill to meet the oil and gas needs in the 2040s and 2050s,” he said.

But managing that growth can be tricky as it hinges, in part, on government regulations. In the US, for example, the most recent 5-year program for leasing federal lands on the Outer Continental Shelf, covering the period from mid-2017 to mid-2022, expired in June 2022. The proposed program for the 2023–2028 period, released by the US Bureau of Ocean Management in July 2022, has not been finalized or implemented.

“It’s important to acknowledge that we’ve already got some leases in hand that we’re working on evaluating and developing. I hope one day that they’ll turn into something that we can bring on stream,” said Rich Howe, executive vice president of deep water for Shell.

“But at a certain point, you work through that inventory, and if there’s nothing else filling the funnel behind, then you’ve got an issue. Continued investment depends on continued leases being available and building the energy system of the future.”

He added that Shell strongly supports lease sales as an essential avenue for expanding the supply of secure and lower-carbon barrels in the US Gulf of Mexico.

“It’s just absolutely vital. As an energy professional and an American, I can say it’s essential. We encourage the current administration to resume offshore leasing and develop the 5-year plan to have runway visibility of what’s coming our way and make capital choices. We can allocate our resources in a way that it gets more stable and predictable,” said Howe.

Keeping the shelves stocked with fresh inventory ensures the project conveyor belt keeps rolling, but Howe noted that this belt is not limited to the Gulf of Mexico.

“It runs through the Gulf of Mexico, but it’s not limited to the Gulf,” he said. “As you begin to have issues in certain parts of that conveyor belt and you’ve resources available elsewhere, you must redeploy to those other places.”

Disturbing Trend

The industry is noticing a disturbing trend of lower discovered volumes. Rystad’s estimates show that in the first half of 2023, explorers found 2.6 billion BOE, 42% lower than the first half of 2022 total of 4.5 billion BOE. Fifty-five discoveries have been made, compared to 80 in the first 6 months of 2022.

This “precipitous drop,” the report said, is due to the strategic shift by the industry to target more-profitable and geologically better-understood regions and to the failure of several critical high‑potential wells.

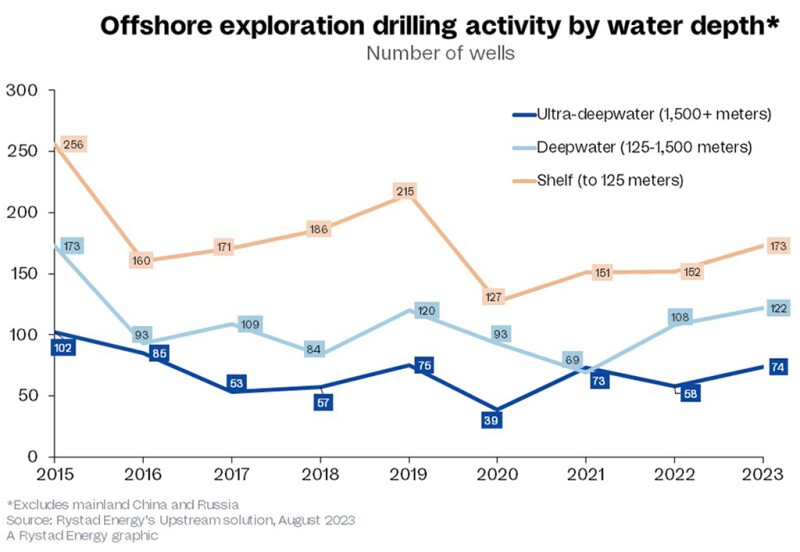

According to the report, the offshore sector has prioritized locating new resources, aiming to capitalize on underexplored or frontier areas where high-risk, higher-cost offshore developments could unlock new volumes.

“Despite accounting for about 95% of exploration spending in 2023, the offshore industry has only contributed to about two-thirds of the total discovered volumes,” the report said.

As governments, industries, and organizations clamor and debate the need for stricter policies and call for increases in capital investment to battle greenhouse gas emissions—be it by planting more trees or sucking carbon out of the air and pumping downhole into depleted offshore fields—one challenge continues to grow.

Yesterday’s elephants, fields holding more than 500 million or more barrels of oil—Ghawar, Prudhoe Bay, and Cantarell, for example—helped build today’s economies and drive population growth, currently at around 8 billion, according to the United Nations. In 2050, the world’s population will reach about 9.7 billion.

In its recent global energy outlook, ExxonMobil said that to support this growing population with rising living standards, the world will need to produce 15% more energy in 2050 than it does today. The supermajor also projected that—even with the rise in lower-emission options—more than 50% of energy demand will still be met by oil and gas in 2050.

While many expect oil and natural gas to retain their roles in the energy mix of 2050, the more significant question should not only be on how much oil and gas will be needed but from where the world will find it.

Where Are the Next Generation of Resources?

Embarking on such a hunt is no easy task—it demands unwavering dedication, potentially extending over decades. Current exploration hotspots dot the coastlines of South America and West Africa and pop up across the Eastern Mediterranean. The Gulf of Mexico’s complex geology also keeps explorers and technology developers busy.

“High-impact exploration will persist as a high priority, especially for the Majors who need to replenish their reserves and generate returns. We are seeing exploration budgets and energy transition projects/initiatives going hand-in-hand,” said Jamie McGreevy, a research analyst, Sub‑Saharan Africa, for Welligence Energy Analytics.

McGreevy noted that the elephant fields “still exist but require stepping out into challenging water depths, applying new geological concepts to already explored regions, or unlocking frontier basins.”

“There have been some huge discoveries in the last couple of years, namely Venus in Namibia, Baleine in Côte d’Ivoire, and not forgetting Guyana,” said McGreevy. “Eni, for example, has stated that the Baleine project marks Africa’s first emissions‑free production project. Residual emissions are offset through initiatives developed within the country, including eliminating the need for wood or coal for cooking. Companies are keen to bring discoveries online as quickly as possible, and managing routine flaring and venting from the facilities/wells is becoming a priority.”

McGreevy said the Eastern Mediterranean will continue to be a hotspot and is currently seeing a lot of drilling, as is the Orange Basin in Namibia and South Africa.

For example, TotalEnergies and partners Eni and QatarEnergy recently spud exploration well 31/1 on Block 9 of Lebanon’s Qana prospect. Reuters recently reported that Namibia holds about 11 billion bbl of oil in recently discovered offshore fields, with TotalEnergies’ Venus-1X find making up almost half the total.

“I believe the success in Namibia will drive conjugate margin exploration in Brazil and Uruguay’s Pelotas Basin,” McGreevy said.

TGS’s Hajovsky said he believes there are still significant discoveries, but the questions and challenges become greater once found.

“TotalEnergies, with its Venus discovery, and Shell, with the Graff discovery offshore Namibia, will be multibillion-barrel fields. The question becomes, ‘what will it take to develop these fields?’” he said.

It is not just the economics that are challenging; so, too, are the technical challenges and what it will take to develop it.

“What do we have in our toolkit as an industry from a technology point of view to maximize that potential,” he said. “Look at what ExxonMobil found in Guyana with Stabroek in 2015. They’re now at more than 11 billion barrels of recoverable resources.”

He noted that TotalEnergies said it will make a final investment decision at its Block 58 prospect offshore Suriname.

“It’s a large field,” he said. “They must find a way to make it economic. Large prizes are still to be had out there, and I think you’ll continue to see exploration move that way.”

Hajovsky said he finds offshore Uruguay very interesting as it is the conjugate margin analog to Namibia.

“We’ll see some wells drilled there to test the concept,” he said. “Offshore Argentina is a largely underexplored area, and a significant well will probably be drilled early next year, which could be a play opener.”

The Equatorial Margin of Brazil is also an area of interest for Hajovsky because “we’re looking for that analog to Guyana. It’s an area with a lot of potential. Petrobras has been very open with their budget, and they’re allocating much capital to explore the Equatorial Margin.”

Gulf of Mexico Aging Gracefully

When compared against the recent discoveries offshore Guyana and Suriname or Namibia and South Africa that were decades in the making, the Gulf of Mexico basin is considered a mature basin that continues to yield new resources.

According to Hajovsky, the Gulf of Mexico is a prime example of how exploration and technology advancements continue to unlock resources.

“Every decade, as technology improves, the basin rediscovers itself with another play type, whether you’re talking about the Pliocene, the Miocene, or the lower Paleogene. Improvements in the quality of seismic data imaging allow you to see new things. As the drilling technology improves, you can test deeper objectives like the 20k high-pressure environments. Technology helps us to discover more in that way.”

One area in which TGS has been doing extensive work is coupling ocean-bottom nodes (OBN) survey data with its proprietary imaging algorithms to improve seismic image quality.

“We collect the data in the field and apply our supercomputing capability to create highly detailed, high-resolution snapshots of the subsurface. Once in the client’s hands, they can identify more resources and resolve uncertainties,” he said.

“A simple way to think about it is to compare a photo taken with a first-generation iPhone against the current generation with the three-camera configuration. You can see how much clearer and crisp the image is. That’s the variation in what we can do with technology today.”

Hess views the Gulf of Mexico as an important cash engine and platform for growth, participating in seven key producing fields and holding more than 85 leasehold blocks. The company’s objective for the basin is to sustain or grow its production through tiebacks and hub-class exploration success.

“Even though the Gulf of Mexico is a mature basin, technology is continuously improving, making it an attractive investment opportunity,” said Tim Cordingley, vice president of exploration North America for Hess. “Enhanced technology has enabled us to image areas in the GoM that couldn’t be confidently mapped before, and this has allowed us to unlock more drillable prospects.”

Cordingley noted that the company has been actively shooting OBN surveys in and around its hubs.

“When coupled with new algorithms, this process allows us to see new opportunities in the subsalt in the Gulf of Mexico,” he said. “These seismic improvements are leading that charge to help us unlock further opportunities in the GoM.”

One such opportunity credited to using OBN technology and full-waveform inversion is Hess’s Pickerel-1 oil discovery on Mississippi Canyon Block 727, which encountered about 90 ft of net pay in a high-quality oil-bearing Miocene-aged reservoir. The infrastructure-led exploration well will be tied back to the Hess-operated Tubular Bells production hub.

Pickerel was the first well of the company’s Gulf of Mexico drilling program for the year. Hess is currently drilling its Black Pearl development well. The well is planned as a tieback to the Stampede production hub about a mile away. Following Black Pearl, the company plans to drill its Vancouver prospect located in Green Canyon Block 287. It is a large hub-class exploration prospect targeting a subsalt Miocene-age reservoir.

Industry activity is increasing in the Gulf of Mexico’s Paleogene as technological advances have enabled work in the play’s challenging conditions.

The industry’s first deepwater high-pressure development in the Paleogene to achieve a final investment decision is Chevron’s Anchor project at Green Canyon Block 807. The field’s semisubmersible floating production unit arrived on location during the summer, and work is progressing to first oil in early 2024.

The delivery of new technology capable of handling pressures of 20,000 psi, such as drillships, blowout prevention systems, and subsea production systems, enabled access to other high‑pressure resource opportunities across the Gulf of Mexico for companies like Beacon Offshore Energy and BP.

Beacon is progressing on its ultrahigh-pressure oil and gas development in the deepwater Gulf at Shenandoah in Walker Ridge Blocks 51, 52, and 53.

BP announced in its second quarter earnings 2023 call that it progressed work on its Kaskida project to concept selection and that they are also evaluating options to progress the Tiber project.

The company's Project 20k was launched in the early 2010s to work on the technology to develop the two Paleogene projects—discovered in 2006 and 2009, respectively—was shelved several years ago during a market downturn.

Kaskida is a "big, big resource, a lot of oil in place. And the question was how to recover it economically. It's a good story, I think, of the company retaining an option. And we retained that option over many, many years," said Bernard Looney, former chief executive of BP, in the earnings call.

"At the same time as us doing that, the industry has moved forward. 20k rigs have been built and are in operation. People have been successful with not just the technical aspects of the developments, but also increasing the learning around how these reservoirs produce. And both of those things are encouraging for us. So we're encouraged by what we see others do," he said.

"We feel that its time has come. It has entered concept select. Unusually, it's 100% BP. Our job now and the team is focused on working through that optimization and getting us to a project that we can develop that's economic, and that's what we're focused on doing.

"At the same time as we're doing that, we're focused on Tiber, which is at an earlier stage in the thinking, so to speak. But if Kaskida enters the frame, there's no reason why Tiber wouldn't also enter the frame."

Shell partnered with Equinor in June 2022 to develop the Sparta field located on Garden Banks Blocks 915, 916, 958, and 959. The field, formerly known as North Platte before TotalEnergies relinquished operatorship and its interest in the field, features a subsalt Paleogene reservoir and will require 20,000-psi technologies to develop.

“While moving into new areas like the Paleogene doesn’t meet the technical definition of frontier, it’s new for us and for a lot of players in the Gulf of Mexico. It’s a new kind of geology, and a new set of drilling and completion and development challenges. We’re super excited about it,” said Howe. “It is still an emerging play in the Gulf of Mexico, and we’re highly active there.”

He said Shell’s exploration strategy in the Gulf of Mexico and beyond is to sustain a healthy pipeline of high-value, near-field, near‑infrastructure, and core discoveries.

“There’s a lot of romance in these big, new, mysterious plays,” he said. “But there’s a lot of value in the stuff that’s right in your own backyard, near the installed infrastructure you’ve got. You can expect us to continue with that strategy in the Gulf of Mexico.”

The exploration prowess of today’s supermajors, majors, national oil companies, and independents, paired with technological advances and capital investment, will deliver the supply needed to meet future energy demand. Doing so will require capital in various forms—financial, mental, physical—and a little wildcatter’s luck and perseverance.