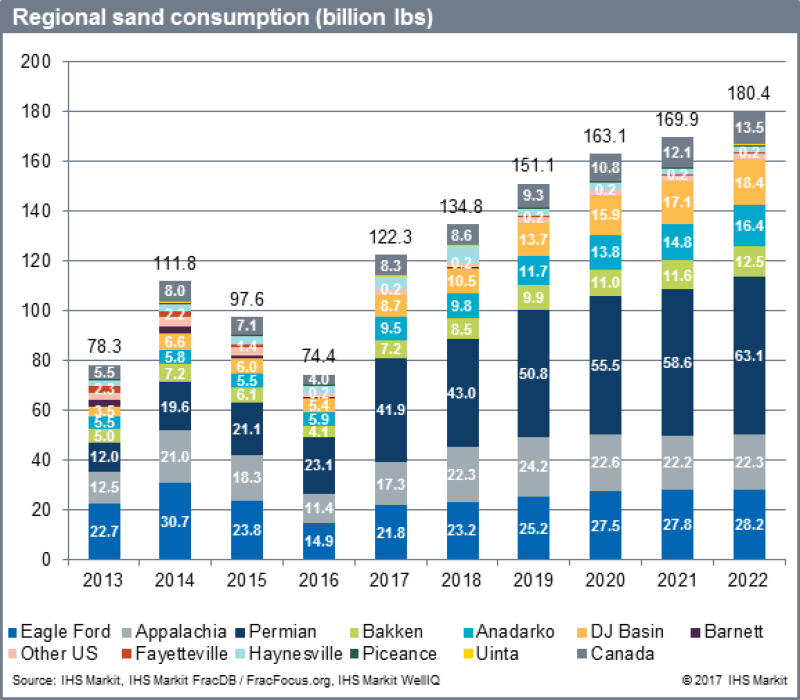

The frac sand sector has re-entered bullish territory in 2017 as demand is expected to exceed peak 2014 levels before the end of the year. Increasing lateral lengths, stage counts, and proppant intensity levels have all contributed to a significant uptick in frac sand consumption. As in many categories, the Permian leads the way and is expected to consume more than twice the amount of frac sand as in 2014, accounting for 37% of total frac sand demand in the US in 2017. In addition to significant demand increases, there are a few interesting trends happening in the frac sand market that we are keeping a close eye on through our ProppantIQ product and research.

An increasing number of operators successfully unbundled services from oilfield service companies and have started self-sourcing or direct sourcing sand through sand mine operators. This trend has been stickier than we had foreseen, and has various implications for oilfield service companies; namely, their ability to drive service price increases in the upturn, and potentially reduced barriers to entry for new sector entrants as the recovery continues.

As operators gain experience handling the logistics of frac sand supply, there may be increasingly less chance that they hand responsibility (and margin) back to oilfield service companies. As the market tightens, and logistics become more complicated, some E&Ps may decide the practice is not worth the hassle.

There has also been increased interest in brown sand (sand sourced primarily in Texas) among operators due to its low wellsite delivery cost in comparison to northern white sand (sand sourced from the Midwest). Demand for brown sand has increased drastically during the downturn, causing sand suppliers to buy into regional mines to stay competitive, and, as a result, a substantial amount of frac sand supply is expected to come on line late 2017 and 2018 through brownfield mine expansions and greenfield projects. With operators currently focused on the near- to medium-term, it remains to be seen if this shift in preference will continue should oil prices rise, and outlooks shift to longer-term productivity.

Along with brown sand demand increases, the shift toward finer-grade sand usage has continued. Finer grades of sand now account for 80% of frac sand consumed compared to 60% of frac sand consumed in 2014. This shift goes hand in hand with operators performing a higher number of completions using slickwater chemistry.

In 2014, coarser grades of sand were in very high demand but that trend has completely flipped over a span of 2 years. Sand mine operators holding sand mines that produce a higher percentage of coarser sand grades have taken a hit, and the future for coarser grades of sand remain uncertain.

With costs as well as productivity the primary drivers of the industry for the near-term, the proppant market, and operators’ shifting preferences within it, will be closely watched by partners and investors alike.

Thomas Jacob is a consultant with IHS Markit. He serves primarily as lead analyst on ProppantIQ–a quarterly market intelligence product that provides analysis, insights, and forecasts for proppant demand, supply, pricing, and logistics for North America. He holds a Master’s degree in operations research & industrial engineering from the University of Texas at Austin and a Bachelor’s degree in mechanical engineering from VIT University in India.

This article was originally published on IHS Markit’s Energy Blog. Reproduced with permission.