IHS Markit released its latest CementIQ report in the wake of OPEC discussions and the effects of coronavirus (COVID-19) on the global economy, which have combined to leave the oil market in an historic state of turmoil.

Even before this upheaval, service companies were preparing for a "down" 2020 and Schlumberger and Halliburton made headlines when they announced a 50% and 25% reduction in fracing hydraulic horsepower (HHP), respectively, to address large amounts of generalized oversupply in the US market. While these cuts seemed drastic at the time, no one could possibly have foreseen that the situation would change to the point where we are now projecting a drop of 66% in total US spuds from Q1 to Q4 2020.

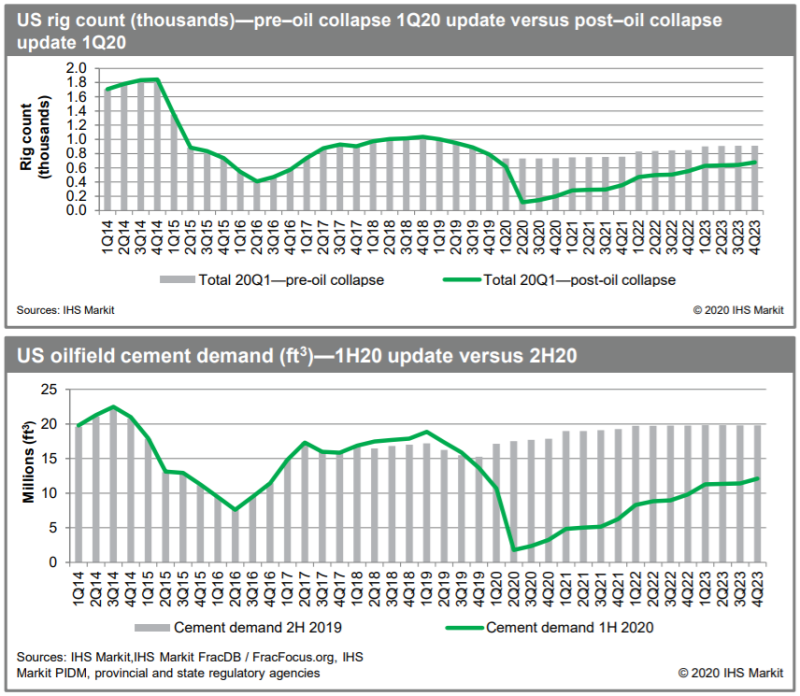

Fracing tends to overshadow cementing in terms of attention, owing to the former's cost and equipment intensity, so you won't hear many such public announcements from service companies for the latter. Nevertheless, our latest research shows that the situation in the cementing market is just as dire as that in the fracing market (Fig. 1).

As a result of the tremendous drop in new well activity and associated cement demand, we expect the cementing services market size in the US to drop 50% year-on-year from 2019, reaching USD795 million in 2020. The significant drop in Permian Basin activity will account for 40% of the total market size reduction.

The decrease in market size expected during 2020 is the result of both the reduction in drilling activity and expected pricing concessions. This will impact service companies most severely: cement and concrete prices are expected to stay relatively flat, so given the drastic decrease in wells spudded as a result of the significant spending cuts announced by operators, service companies are on the hook for any pricing concessions, which will of course cut into their margins.

Unfortunately, many oilfield services have already been giving concessions since the last downturn of 2014–2015, so a survival strategy is not evident at all with even less revenue per job and a drastically reduced job count.

For now, companies are idling equipment which will buy them some time (though it will also hammer their efficiency metrics) but this is not a long-term solution and this only addresses the issue of activity; the effects that COVID-19 could impose on the field crews and their efficiency present an entirely new set of challenges.

Indeed, we can talk at length about the market factors resulting from COVID-19 but we should always remember that this disease puts people at great personal risk. In a service line that requires crews to work closely together for long stretches of time, there are numerous potential implications to consider:

- What happens to efficiency once social distancing takes effect at service locations?

- Will crews be as effective and motivated?

- What happens in the event of a crew fatality caused by COVID-19?

What preparations do suppliers have in place to deal with the emotional and psychological consequences of such an event?

The answers to these questions are difficult to quantify and will likely only become clear well after COVID-19 has run its course. Nevertheless, we will do what we can to report on the disease's effects on cementing suppliers in future publications of CementIQ. For more information, visit www.ihsmarkit.com.