We talk about “the energy transition” as if it were some type of unified, global event. Instead, numerous approaches to energy transitions are taking place in parallel, with all of the “players” moving at different paces, in different directions, and with different guiding philosophies. Which companies are best positioned to survive and thrive, and why? This article takes a look at what several top energy research and business intelligence firms are saying.

What a Difference a Year Makes

Prior to 2020—in fact, as recently as the 2014 bust that followed the shale boom—the oil and gas industry weathered downturns by “tightening their belts” and “doing more with less” in the form of cutting capital expenditures and costs, tapping credit lines, and improving operational efficiency. Adopting advanced digitalization and cognitive technologies as integral parts of the supply chain from 2015 to 2019 led to significant performance improvements as companies dealt with “shale shock.”

Then, in 2020, a strange thing happened. Just as disruptive technologies like electric vehicles and solar photovoltaic and new batteries were gaining traction and decarbonization and environmental, social, and governance (ESG) issues were rising to the top of global social and policy agendas, COVID-19 left companies with almost nothing to squeeze from their supply chains, and budget cuts had a direct impact on operational performance and short-term operational plans. To stabilize their returns, many oil and gas companies revised and reshaped their portfolios and business strategies around decarbonization and alternative energy sources. The result: The investment in efforts toward effecting energy transition surpassed $500 billion for the first time in early 2021 ($501.3 billion, a 9% increase over 2019, according to BloombergNEF) despite the economic disruption caused by COVID-19.

According to Wood Mackenzie, carbon emissions and carbon intensity are now key metrics in any project’s final investment decision. And, Rystad Energy said that greenhouse-gas emissions are declining faster than what is outlined in many conventional models regarded as aggressive scenarios. In Rystad’s model, electrification levels will reach 80% by 2050.

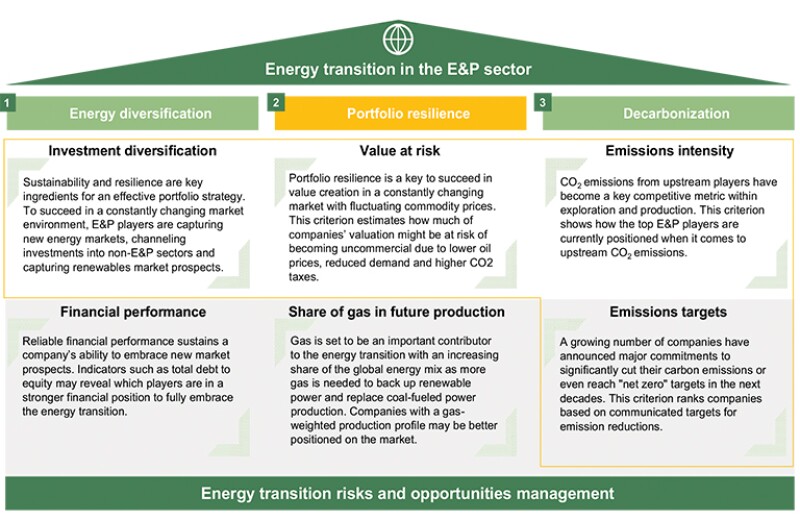

A Look at the Playing Field: Energy Transition Pillars

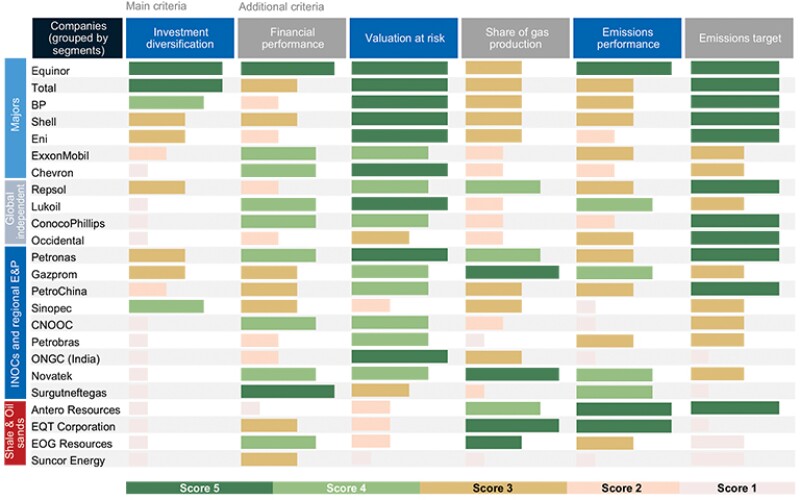

In a February 2021 webinar, Rystad discussed what leading exploration and production (E&P) companies are doing to keep up with the energy transition and stay investable in the rapidly changing market environment. The consulting firm researched the top 25 E&P companies based on their oil and gas production in 2020 and analyzed how they approach various market criteria in “three pillars of energy transition in the E&P sector” that the firm regards as key distinguishers and important indicators of potential success (Fig. 1). The research excludes national oil companies (NOCs) except for those with international activity (INOCs). Rystad says these 25 companies are responsible for almost 40% of global hydrocarbon production and the same share of global E&P investments and believes the trends within this peer group are representative on a global scale.

Energy diversification criteria include investment diversification among new energy markets, non-E&P sectors, and renewables, and reliable financial performance such as total debt to equity, to see which players are in a stronger financial position to fully embrace the energy transition. Over the past 5 years, more upstream companies have increased investments in clean energy across the electricity value chain, but specific investments vary with company types and core markets. For example, Asian INOCs have the greatest share of investments related to non-E&P segments. However, much of this is directed at their midstream and downstream businesses and is therefore still fossil-fuel-related.

Another driver Rystad evaluated to determine investment diversification was renewable power capacity under ownership by 2030. Despite the fact that investments in renewable energy have historically yielded much lower returns than conventional oil and gas projects, this hasn’t necessarily been the truth in recent low-price oil markets as evidenced by Equinor’s earning more from renewables than it did from oil and gas E&P in the first quarter of 2021.

To determine the leaders in investment diversification, Rystad compared E&P companies’ share of non-E&P investments over the past 5 years along with their renewables capacity by 2030. European E&P companies are taking the lead here with ambitious plans for renewables, as their path to energy transition lies with investments in the low-carbon energy systems of the future.

The Rystad webinar touched on two energy transition pillars—portfolio resilience and decarbonization. Portfolio resilience includes value at risk—that is, how much of a company’s valuation might be at risk of becoming uncommercial as a result of lower oil prices, reduced demand, and higher CO2 taxes—and share of gas in future production. Companies with mature portfolios have lower risks. Shale and oil sands companies have higher risks and are more heavily geared to oil price.

Gas is set to be an important contributor to the energy transition with an increasing share of the global mix as more gas is needed to back up renewable power and replace coal-fueled power production. Companies with a gas-weighted production profile may be better positioned in the market, according to Rystad.

Decarbonization includes emissions intensity, flaring, and emissions targets based on companies’ communicated targets for emissions reduction. Occidental was praised as being ambitious for doubling down on carbon capture and storage (CCS) efforts to reach net zero.

Fig. 2 displays the firm’s final energy transition scores for its researched companies, organized by type.

Long-Termists and Short-Termists

Industry technical advisory and analytics firm DNV conducted research with more than 1,000 senior industry professionals from 79 countries in late 2020 for its outlook for oil and gas in 2021. The participants came from across the oil and gas value chain, including both publicly and privately held companies, and represented functions from board-level executives to senior engineers.

“There is a massive strategy reorientation happening that will lead to moves in different directions,” said Eirik Wærness, senior vice president and chief economist of Equinor. “Companies are not all going to do the same things in the energy transition space—some will do more solar, some will go with onshore wind, some offshore wind, others will invest in hydrogen or CCS, and so forth. You’ll see transactions firming up the basis for those types of strategy movements.”

DNV’s Outlook for the Oil and Gas Industry in 2021 forecast that policy-driven transitions in Europe, North America, and China will lead the decarbonization of the world’s energy system.

According to the DNV survey, 66% of respondents said their organizations were actively adapting to a less carbon-intensive energy mix in 2021—up from 44% in 2018. Like Rystad, the DNV survey revealed that the pandemic has had a catalyzing effect on energy transition, making climate change an even more important strategic driver for a growing number of organizations. Organizational strategies will depend on how much change companies perceive and expect, and how fast they believe the world will transform in 2021 and beyond, reported DNV.

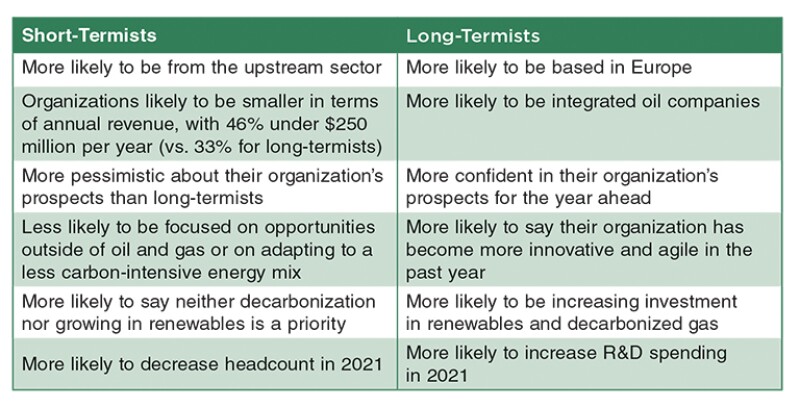

Based on survey responses, DNV believes the industry will see a split between two broad groups in the industry—long-termists and short-termists—defined by their size, location, and confidence levels and leanings toward two opposing strategies. The long-termists will continue to transform for the future while the short-termists will focus on thriving or just surviving on more traditional opportunities. The situation will be fluid, with some organizations switching between one strategy and the other, while others try to balance their strategies for all time horizons (see table).

Leveraging Competitive Advantage

Wood Mackenzie, reporting in March on Big Oil’s Separate Paths to Decarbonisation, said, “The pressure to shift from a defensive position on decarbonization to net-zero growth is only going to increase as US climate policy shifts decisively and ESG demands from stakeholders intensify.”

“The US majors ‘get’ decarbonization,” the consultancy said. “They’re now more open about the challenges of the energy transition and how they intend to deal with them.”

The foremost competitive advantage for the US majors, it added, is what they already do. Their goal is to make the integrated oil and gas business more sustainable by reducing methane intensity and eliminating routine flaring in upstream, sourcing renewables to power operations, and shifting the product slate in refining and chemicals to biofuels, lightweight plastics, and innovative new materials.

“The EuroMajors’ master plan goes beyond getting to net zero to ensure a viable and growing energy business when oil and gas fall out of the mix,” Wood Mackenzie said, and concluded, “Strategy for legacy oil and gas is broadly the same in Europe and the US, but European majors have chosen to take on the risks of building a broad-based new energy business in parallel with renewables as the starting platform.”

What Determines a Winner?

Wood Mackenzie has asked rhetorically, “Are US majors doing enough to decarbonize, or are EuroMajors pushing too hard, too fast into new energy?” and answered, “With investors, the jury is still out. After a tumultuous 12 months where share prices were whiplashed by the oil-price collapse and recovery, and BP and Shell cut dividends, it’s not clear either strategy is winning—yet.”

Rystad has advised that it is important to keep in mind that priorities may differ depending on the markets in which companies operate. Investments in renewables is an inseparable part of the energy transition strategy for European majors, but not for Asia-focused players. In Asia, gas production is a more important ingredient in the energy transition because gas can substitute for coal and fuel oil in many Asian countries.

“There is therefore no single, perfect strategy to ‘win’ the energy transition,” said Rystad.

For Further Reading

Rystad Energy. Upstream Webinar: Which E&P Company is Best Positioned for the Energy Transition?

DNV. Turmoil and Transformation: The Outlook for the Oil and Gas Industry in 2021

Wood Mackenzie. Big Oil’s Separate Paths to Decarbonisation