Despite positive geopolitical developments, an increase in progressive policies over the past 18 months, and the impending fall of global emissions, the energy transition is “still in the starting blocks,” according to DNV’s 2023 Energy Transition Outlook.

“Globally, the energy transition has not started, if, by transition, we mean that clean energy replaces fossil energy in absolute terms,” said Remi Eriksen, group president and CEO of DNV. “Clearly, the energy transition has begun at a sector, national, and community level, but, globally, record emissions from fossil energy are on course to move even higher next year.”

The annual report highlighted six key developments, including the effect of energy security concerns, inflation, supply chain disruptions, and progressive policies in some regions.

- The transition is still at the starting blocks. As global energy-related emissions continue to climb with an anticipated peak in 2024, surges in new oil and gas projects and disruptions in the oil market are driving emissions higher and are forcing a delay in the beginning of the transition.

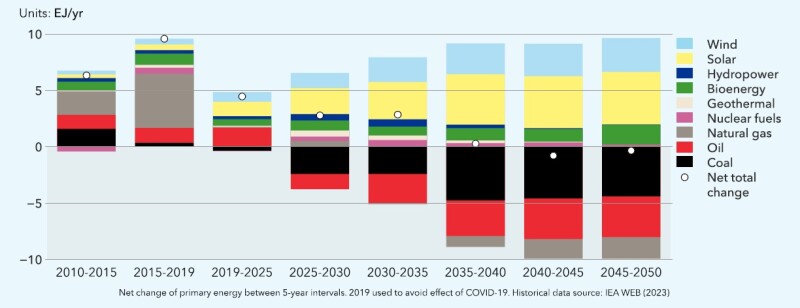

- Renewables outsprint fossils from the mid-2020s. Because the transition involves the addition of renewables and the removal of fossil sources (Fig. 1), it is expected now to take the next 27 years to move the energy mix to 48% fossil fuel and 52% nonfossil fuel. Wind and solar power are expected to grow tenfold and 17-fold, respectively, between 2022 and 2050. From 2025 on, almost all new capacity will be nonfossil.

- Energy security is moving to the top of the agenda. Price shocks for energy importers, supply chain complexities, inflation, and the disruption of energy supplies are among the causes for an increased focus on energy security. Locally produced energy is becoming more sought after than energy imports, with DNV estimating the willingness of governments to pay a premium of between 6 and 15% for locally sourced energy.

- Progressive policy is having an effect. Major policies, including the US Inflation Reduction Act and the EU’s Green Deal, REPowerEU, and Fit for 55 policies, are helping to accelerate the transition. As countries progress in “the race to the top,” developments in clean energy, including hydrogen and carbon capture and storage, will drive global learning benefits.

- Gridlock impedes the near-term expansion of decarbonization technologies. DNV reported transmission and distribution grid constraints are emerging as the key bottleneck for renewable electricity expansion and related distributed energy assets such as grid-connected storage and electric vehicle charging points among several countries. Expropriation and financing to ease cable manufacturing production constraints are potential solutions to address the gridlock as countries seek policies to fix permitting delays.

- Global emissions will fall, but not fast or far enough. DNV forecast global energy-related CO2 emissions in 2050 will be 46% lower than today and, by 2030, only 4% lower than they are today. Using 2.2°C of global warming above preindustrial levels as part of the forecast, DNV reported that limiting global warming to 1.5°C is more unlikely than ever before.

“There are short-term setbacks due to increasing interest rates, supply chain challenges, and energy trade shifts due to the war in Ukraine, but the long-term trend for the energy transition remains clear: The world energy system will move from an energy mix that is 80% fossil-based to one that is about 50% nonfossil-based in the space of a single generation. This is fast, but not fast enough to meet the Paris goals,” Eriksen said.