The US ramped up its LNG liquefaction capacity in 2022 becoming No. 1 in the world by adding 88.1 mpta to its previous year capability, a figure representing 75% of global growth in liquefaction capacity, according to the London-based International Gas Union’s (IGU) 2023 World LNG report.

Released at its triennial conference, held this year in July in Vancouver, Canada, the report noted that worldwide LNG operational capacity rose 4.3% (478.4 mpta) year-on-year with European buyers importing 66% more LNG last year than in 2021, with the US pushing to be first in line to satisfy transAtlantic demand.

Among the 2022 highlights from the IGU report were:

- Europe approved record new regasification capacity and utilized floating regasification and storage options to bring some of that capacity online in record time.

- Since the start of the war in Ukraine, more than 10 European markets—among them Germany, the Netherlands, Finland, France, Croatia, and Italy—have started to construct new infrastructure.

- Europe-bound US LNG exports jumped 148% over 2021 levels, hitting 55.2 mt, despite Freeport LNG in Texas being taken offline in June 2022 because of an accident.

- LNG volumes from the US accounted for 44% of Europe’s total LNG imports while Europe accounted for 69% of total US LNG exports.

- The two fastest-growing LNG markets, China, and India, reduced imports by 19.3% and 17.7%, respectively.

- Qatar and Russia joined the US as Europe’s top three LNG suppliers with more than 70% of Europe’s LNG imports coming from those three countries.

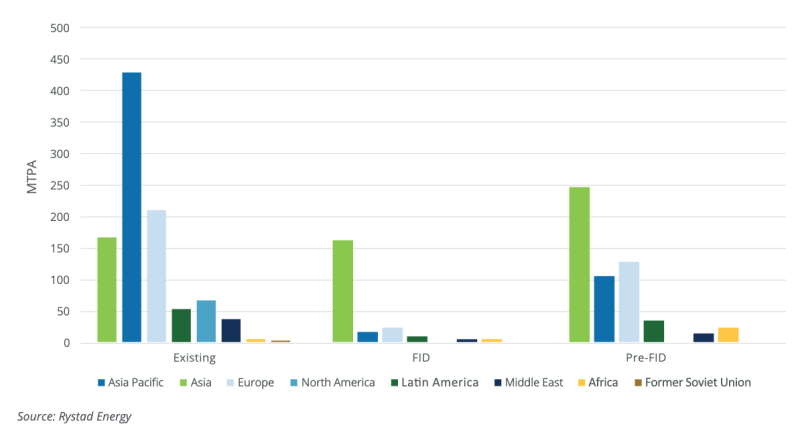

Global liquefaction capacity by region and status, end April 2023

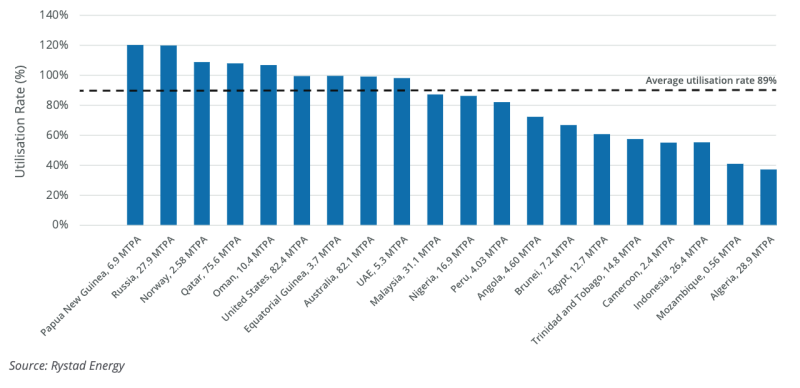

Global liquefaction capacity utilization, 2022 (capacity is prorated

While Europe was shunning Russian pipeline gas in 2022, it was at the same importing record volumes of Russian LNG—20% more than it had in 2021. The trend has continued into 2023 with Russian LNG exports to Europe in the first 6 months of this year on a par with year-ago volumes—about 9 mt, Reuters has reported, citing Refinitiv Eikon data.

In the same January to June 2023 period, total Russian LNG exports dropped overall by 9.4% to around 14.4 mt as its Asia-bound cargoes fell to 5.2 mt as compared to 7 mt in the same period a year ago, the Refinitiv Eikon data revealed.

More Long-Term Offtake Agreements Lead to More Projects Reaching FID

With security of supply top of mind, LNG buyers seem keen now to negotiate long-term contracts as opposed to spot market purchases, which had been the norm in recent years.

The result has been an uptick in positive final investment decisions (FID) on newbuild and facility expansions, which depend on the depth and breadth of offtake deals to secure financing that would need to be repaid over a period of years.

Of the LNG offtake contracts signed in 2022, 90% were for 15 years or more while 65% exceeded 20 years, the IGU found. Moreover the 70 mt of LNG spoken for in those agreements was more than double the average of the preceding 5 years.

US exporters dominated the sellers’ side last year while China and LNG aggregators commanded buy-side activity. By building up global LNG portfolios, aggregators drive future demand by increasing supply; they in effect open and build up new markets which may lack the buying power to sign a long-term commitment initially but can ease into the market by offtaking a portion of an aggregator’s portfolio.

The IGU noted, however, that Europe sourced 70% of its 2022 imports from the spot market.

Europe Dominated LNG Markets

Utilization of European regasification facilities hit record highs of 65% in 2022 as compared to 41% in 2021, with many European markets maxing out import capacities.

France’s LNG import terminals ran at full capacity through most of the year while Belgium’s terminals clocked an average utilization rate of 142% over 2021.

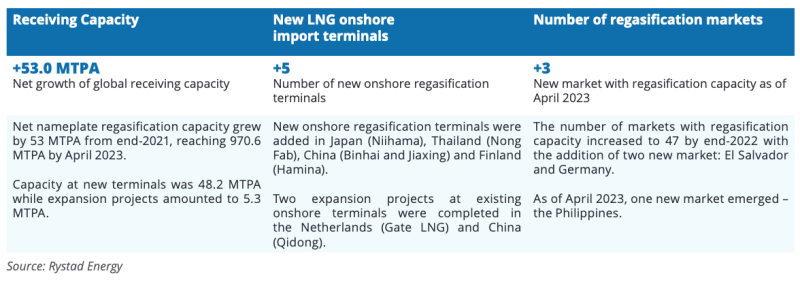

Europe has launched 26 regasification projects with an overall capacity of 104.5 mpta with floating terminals accounting for nearly 70% of that new capacity. Six of the 26 have been commissioned, adding 25.5 mpta to global capacity as of April 2023, according to the IGU.

Four projects with a combined capacity of 18.8 mpta are under construction with the remaining 16 in various planning stages.

Germany plans to add the highest volumne of regasification capacity among European markets, a projected 41.54 mpta, by building terminals at Wilhelmshaven, Lubmin, Brunsbuettel, and Stade by 2026.

Germany’s regasification capacity is expected to meet over 60% of its gas demand once all terminals have started operating.

New LNG regasification terminals worldwide, January 2022 to April 2023

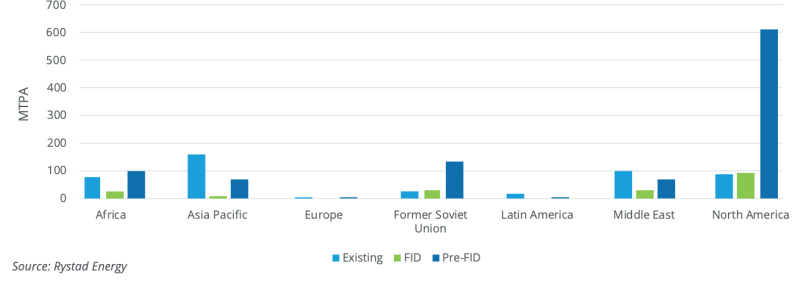

LNG regasification capacity – FID and FEED by status and region, April 2023