This is the second of a series of six articles on SPE’s Grand Challenges in Energy, formulated as the output of a 2023 workshop held by the SPE Research and Development Technical Section in Austin, Texas.

Described in a JPT article last year, each of the challenges are discussed separately in this series: geothermal energy; net-zero operations; improving recovery from tight/shale resources; digital transformation; carbon capture, utilization, and storage; and education and advocacy.

The first article, “An SPE Grand Challenge Update on Geothermal Energy,” was published in April 2024.

At COP28, more than 50 oil and gas companies, many of them national companies, took a historic step toward decarbonization by launching the Oil & Gas Decarbonization Charter. The charter represents significant short- and long-term ambitions to reduce emissions, including net-zero operations by 2050 at the latest.

This article explores the importance of this effort, the opportunities available to the industry to reduce its Scope 1 and 2 emissions, and the key technologies needed to achieve the net-zero goal.

The Size of the Prize

According to the latest data from the International Energy Agency (IEA), the production, transport, and processing of oil and gas resulted in 5.1 GtCO2e in 2022. These emissions stem from the production and delivery of oil and gas and the combustion of fossil fuel necessary for operations on-site (Scope 1), and the import of electricity from external sources consumed in oil and gas facilities (Scope 2).

These Scope 1 and 2 emissions represent just under 15% of global energy-related greenhouse gas (GHG) emissions. This is a sizable contribution, nearly equivalent to all energy-related GHG emissions from road transport, highlighting the relative scale of the opportunities associated with implementing operational changes in the industry. The faster and deeper these emissions reductions are, the more significant the impact will be.

Sources of Emissions

To understand the various paths to net zero an oil and gas company can follow, it is critical to map the sector’s sources of emissions throughout the value chain. It is generally recognized that around 60% of an integrated company’s emissions emanate from upstream operations, predominantly from onshore assets. Refining and distribution are the second main contributors, but of a smaller order of magnitude, notably because of significant efforts already made by companies to reduce emissions from their refining assets and levers of decarbonization potentially easier to implement.

However, emissions volumes and intensities differ significantly across regions, countries, and asset types. An asset operating in the Canadian oil sands region will have a very different emissions profile compared to an offshore platform in Western African countries. These differing profiles also call for tailored emission-reduction approaches. This means decarbonization studies must be carried out at the asset level, allowing operators to identify the most cost-effective means of tackling emissions reduction.

Key Technologies To Reach Net-Zero Operations

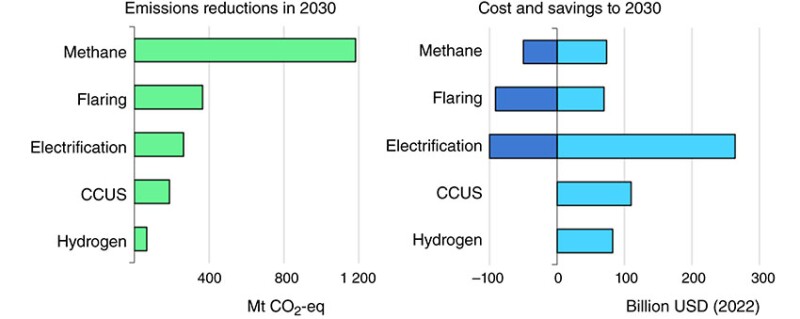

The majority of operational emissions can be addressed through the application of five broad options:

(1) Reducing methane emissions

(2) Eliminating nonroutine flaring

(3) Electrifying upstream facilities using low‑emissions power sources

(4) Equipping oil and gas processes with carbon capture, utilization, and storage (CCUS)

(5) Expanding the use of low-carbon hydrogen in refineries

The first three are believed to be the most readily actionable and cost-effective measures available, notably where pre-existing infrastructure can be easily adapted. For example, if a company already operates a gas network, applying appropriate processes and hardware to reduce methane emissions can lead to higher retention of revenue-generating product and an increased return on investment.

Despite the ease of implementation of some of these decarbonization levers, IEA estimates that these five sets of solutions may require close to $600 billion of cumulative spending over the next decade (Fig. 1).

Reducing Methane Emissions: A Shift in Mindset

Methane, although shorter-lived than CO2, possesses a significantly higher warming potential—estimated to be around 28 times more potent than CO2 over a 100-year horizon. These emissions originate across the natural gas value chain from production to transmission. Most notably they arise from venting, leaks (fugitives), and inefficient flaring, and represent around half of the oil and gas industry’s total operational emissions. This means reducing these methane emissions offers one of the strongest short-term opportunities to advance the goals of the Paris Agreement.

Recognizing this, the signatories of both the Aiming for Zero Methane Emissions Initiative and the Oil & Gas Decarbonization Charter have committed to near-zero upstream methane emissions. These initiatives aim to eliminate the oil and gas industry’s methane footprint by 2030 by treating methane emissions as seriously as the oil and gas industry already treats safety. That is, aiming for zero and striving to do whatever is needed to get there. They also complement other key industry initiatives such as the Methane Guiding Principles (MGP), the Oil and Gas Methane Partnership 2.0 (OGMP2.0), and the Global Methane Pledge.

How To Eliminate Methane Emissions

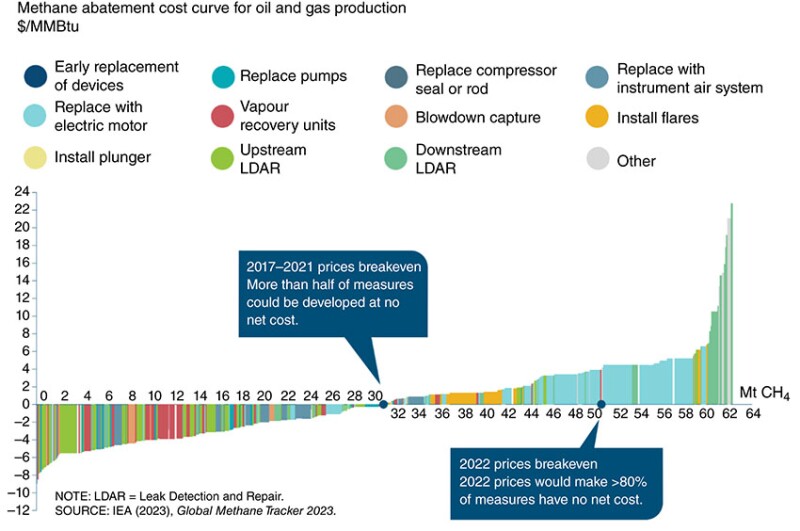

From satellites and drones to seals and pumps, technologies to detect and mitigate methane emissions are evolving rapidly, with some already technically proven and deployed. However, their costs vary depending on a number of factors, including technologies, practices, geographies, asset densities, and remoteness.

As shown in Fig. 2, the IEA estimates that at least 75% of methane emissions from oil and gas operations today can be abated with existing technology. Despite such optimism, challenges to emissions reduction remain, including information gaps, missing infrastructure, and economic barriers.

A comprehensive buildout of gas-handling infrastructure is critical for enabling solutions at low cost. Further, collaboration within the industry, such as the Oil and Gas Climate Initiative (OGCI) and MGP’s efforts to bring companies together to work on emissions reduction efforts, coupled with clear regulatory support—for monitoring, reporting, and verification of emissions for instance—can remove obstacles around methane mitigation.

Eliminating Nonroutine Flaring

Depending on its efficiency, flaring releases both methane emissions and CO2 because of the incomplete combustion of the natural gas. Although it is estimated that flaring efficiency typically falls between 95 and 98%, inefficient flares could allow from 10 to 15% of the gas to be released into the atmosphere.

The World Bank produces an annual Global Gas Flaring Tracker which estimates that around 140 billion m3 of gas was flared in 2022. This is equivalent to the total annual natural gas exports from Qatar, the world’s third-largest gas exporting country that year, considering data from Statista. This large volume translates to more than 350 MtCO2e. IEA estimates that approximately 70% of the flared gas is from flares that operate on a near‑continual basis.

Nearly 95% of the GHG emissions arising from flaring are addressable with existing technologies, including distribution to consumers, reinjection of flared gas to support reservoir pressure, or conversion to LNG. Although the cost of eliminating flaring can vary widely, it could potentially save billions of dollars in avoided emissions at current carbon price levels.

At COP28, the World Bank launched the Global Flaring and Methane Reduction (GFMR) Partnership, a new multi-donor trust fund focused on helping developing countries cut CO2 and methane emissions generated by the oil and gas industry. Committed to ending routine gas flaring at oil-production sites globally and reducing methane emissions from the oil and gas sector to near zero by 2030, GFMR will provide more than $250 million and mobilize significant funding from the private sector to support those countries with the least capacity and fewest resources to address these emissions.

Electrifying Upstream Facilities With Low-Emissions Electricity

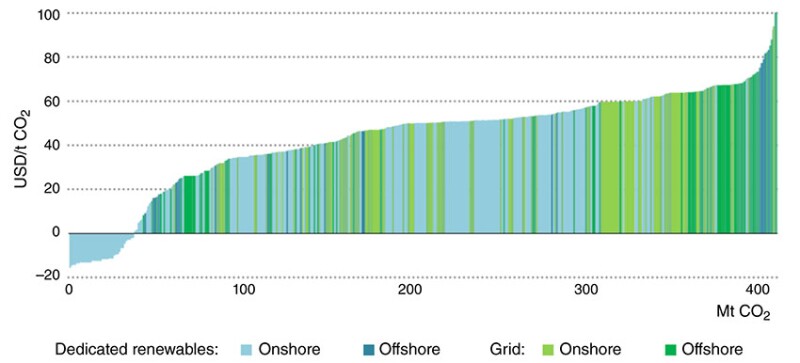

Internal combustion engine generators are a common sight in upstream facilities and replacing them with electricity supplied by low-carbon sources provides an immediate emissions-reduction benefit. The prize for reducing emissions through this measure is also significant as it directly addresses a large source of Scope 1 emissions from the upstream sector.

The energy for upstream facilities could be provided by electricity from a centralized grid or generated in a decentralized renewable energy system. Operators face several choices when implementing an electrification program, including selecting the appropriate technology and assessing total costs. Continuity and reliability of the power source is also critical for safety considerations.

The industry has a long and successful track record in this area, with several projects up and running for over 20 years. Power generated from onshore facilities has dominated the project pipeline, and electrification of offshore assets will be more complex, with the cost of this measure ranging from hundreds of millions to billions of dollars, depending on the scale of implementation and the availability of low-cost renewable energy. Electrification of plants that are already in operation requires major retrofitting and is mainly economical for plants with long lifespans ahead (Fig. 3).

Carbon Capture, Utilization, and Storage (CCUS)

CCUS technologies capture CO2 emissions from the combustion or conversion of fossil fuels and then either store it in subsurface geologies or convert it into useful products. This strategy is primarily a tool for the downstream sector, but applications can also be found in the midstream and upstream sectors. The cost of implementing CCUS technologies can be high, in some cases totalling billions of dollars, but the potential impact is also substantial, as it offers a way to significantly reduce the sector’s downstream emissions.

The oil and gas industry has long been at the heart of CCUS development globally with more than 40% of CCUS investments since 2010 directed towards projects related to oil and gas value chains, according to the IEA. Importantly, knowledge and skills developed in this area are expected to benefit industries beyond the oil and gas sector as carbon capture technology matures.

One of the key challenges is understanding and communicating metrics and costs. To accelerate the development and adoption of CCUS globally, OGCI has created the Global CCUS Hub Search that provides high-level information on potential economic hubs.

Expanding the Use of Low-Carbon Hydrogen in Refineries

According to the IEA, more than 40 million tons of hydrogen is used every year to refine and upgrade oil in refineries—almost two-thirds of it from natural gas or coal—resulting in almost 400 MtCO2e of emissions. Replacing natural gas used in refining processes with low-carbon hydrogen can significantly reduce emissions from the downstream sector. The cost of implementation can be quite high, especially for initial capital investments. The economics will be best in regions where imported natural gas prices are relatively high and renewable electricity costs are relatively low. But the benefits are also expected to reach beyond the net-zero ambition of the industry by creating the means of meeting an emerging global demand for low-carbon hydrogen.

The industry can play a crucial role in supporting large-scale market expansion of key components in the production of low-carbon hydrogen, including CO2 capture, electrolyzers, energy storage, and other equipment. Based on years of experience producing and handling hydrogen, the oil and gas industry is well positioned to drive its use for operational decarbonization, as the industry applies the skills and resources necessary to scale up those technologies.

Conclusion

Achieving net-zero operations in the oil and gas sector is a daunting task, but not an impossible one. By focusing on reducing emissions, particularly methane, and leveraging technologies like CCUS and low-emissions hydrogen, the industry has the tools it needs to successfully make this transition. It has many of the skills and resources required to scale up decarbonization technologies at its disposal, including global presence, subsurface knowledge, and major project management capabilities. The industry can play a crucial role in supporting large-scale market expansion for carbon capture equipment, electrolyzers, and energy storage installations to accelerate decarbonization.

Delivering on the ambition of net-zero operations is a grand challenge indeed, and success will require both continued investment and innovation from industry, matched with robust policy support.

Disclaimer: The contents of this article are intended to be informative and do not necessarily reflect an official endorsement by OGCI or its member companies.

OGCI is a voluntary, CEO-led oil and gas industry initiative comprising 12 of the world’s leading energy companies, producing around a third of global oil and gas. OGCI focuses on leading the industry’s response to climate change and accelerating action toward a net-zero future consistent with the Paris Agreement. To achieve these ambitions, OGCI members are targeting net-zero emissions at their own operations and collaborating with partners across the industry and in other sectors to urgently reduce global greenhouse-gas emissions. Since 2017, OGCI’s member companies have collectively reduced their upstream methane emissions by 50% and upstream carbon intensity by 21%. To support companies outside the group, OGCI focuses on partnering, capacity building, and innovations to target key technologies and areas that can have the greatest impact on emissions reductions. OGCI’s current focus areas include carbon capture, utilization, and storage (CCUS), methane-emissions reduction, and tackling transport emissions.

For Further Reading

COP28 UAE | COP28 Delivers Historic Consensus in Dubai To Accelerate Climate Action

World Energy Outlook 2023, International Energy Agency

Emissions from Oil and Gas Operations in Net-Zero Transitions, International Energy Agency

Fossil Fuel in Transition: Committing to the Phase-Down of all Fossil Fuels, Energy Transitions Commission

Eliz Ozdemir is a program manager at the Oil and Gas Climate Initiative (OGCI), focusing on the Oil & Gas Decarbonization Charter (OGDC). In this role, she supports the implementation of the OGDC goals, and works closely with the OGDC signatories and external partners to drive forward net-zero solutions. Before her current role, Ozdemir spent several years in the strategy and policy team, where she led various projects on topics related to methane emissions reduction, decarbonization pathways, net-zero strategies, transparency/reporting, and natural climate solutions. She holds an MSc in climate change management and finance from Imperial College London.

Justine Roure is the vice president of OGCI’s Strategy and Policy team. She is responsible for coordinating actions and commitments of member companies and providing strategic direction to the organization on various topics within OGCI. She has more than 15 years of experience in climate change and sustainability, working both at strategic and operational levels. Previously, she worked in consulting where she assisted private and public players in setting up and implementing low-carbon strategies. Roure holds an engineering degree in energy from École Centrale de Lyon.